Fundamental Report

Supply-Side Takeaway: Overall, the domestic surplus of steel in the US is intact, resulting in downward pressure on prices. Looking forward, the upside/downside price risk is moving into balance and the domestic – global differential is primed to turn negative – historically this a strong signal for an impending domestic rally in price, with only a few exceptions.

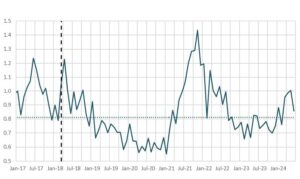

Imports and the Domestic – Global HRC price differential continued to contract, now at the tightest spread since September 2023. This week’s convergence was the result of the domestic spot price dropping, while the global average remained relatively flat. On the imports side, this week’s preliminary data show June arrivals receding from their early month estimate, but the current estimate is still above the long-term average. Additionally, May’s import census data came in, and shows that imports were just above 1M st./m. Finally, domestic production ticked back up again after scaling back for two consecutive weeks. Since mid-January, raw production level has held above 1.7m net tons level.

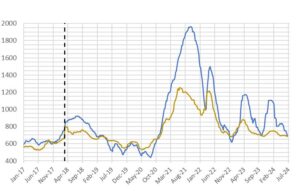

HRC Spot Prices – US Domestic & Global

HRC Spot Prices – US Domestic & Global

- The global HRC spot price rose slightly to $687. Europe was the only country with a price increase, rising by $4. China and Korea fell by -$1.

- The Domestic – Global HRC spread contracted this week, narrowing from $29 to $8.

Total Sheet Imports (s.ton)

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for June indicate an easing for imports, declining to 857k tons from May’s estimate figure of 1004k.

- Potentially seeing that the impact/roll over from the shipping delays have begun to subside.

Domestic Production (s.ton)

Domestic Production (s.ton)

- For the week ending on June 22nd, capacity utilization ticked up by 0.3% to 77.0% and domestic raw steel production climbed to 1.710m from 1.704m/tpw.

- This brings the year-to-date production to 42.204m, operating at a rate of 4%, -2.7% below this point last year.