Fundamental Report

Supply-Side Takeaway: Imports and production remain elevated, but both appear to be retreating. While there is additional room to the downside for domestic pricing over the next couple of weeks, we are quickly approaching a negative global price differential and thus the first fundamental signal of support for the domestic market.

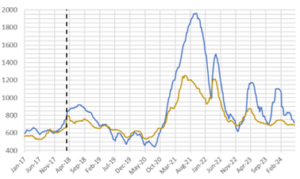

The Domestic – Global HRC price differential continued to contract, reaching the lowest since early-October 2023. This week’s convergence was mainly due to the domestic spot price notably dropping, while the global average broke out below its $4 price range where it had been stuck over the last ten weeks. For imports, the preliminary data for June arrivals indicates a still elevated level compared to the long-term average. However, the revised estimate is lower than last week’s data. The May import estimate maintains to be just above 1M st./m. Meanwhile, domestic production retreated for the second consecutive week, nearing the 1.7m net tons level.

HRC Spot Prices – US Domestic (blue) & Global (gold)

HRC Spot Prices – US Domestic (blue) & Global (gold)

- The global HRC spot price declined to $686. This week all watched countries, except for Brazil, had price decreases: Europe -$16, China -$14, Turkey -$11, Korea -$7, and Russia -$6.

- The Domestic – Global HRC spread contracted this week, narrowing from $45 to $29, its lowest level since early October 2023 after briefly turning negative in September.

Total Sheet Imports (s.ton)

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for June indicate an easing for imports, declining to 903k tons from May’s estimate figure of 1046k.

- Potentially seeing the impact/roll over from the shipping delays caused by the supply chain disruptions.

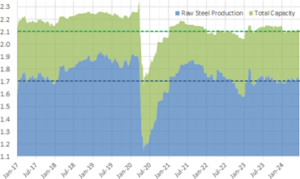

Domestic Production (s.ton)

Domestic Production (s.ton)

- For the week ending on June 15th, capacity utilization took another step lower by 6% to 76.7% and domestic raw steel production declined to 1.704m from 1.716m/tpw, its lowest level since April.

- This brings the year-to-date production to 40.494m, operating at a rate of 4%, -2.8% below this point last year.