Fundamental Report

Supply-Side Takeaway:

Global prices have stalled out and falling domestic prices have caused the U.S. – Global HRC spread to converge to its tightest level since mid-February. Imports data remains subdued and weekly domestic production ticked lower again this week. Given the recent reduction in supply and our outlook of stable to seasonally higher demand in the 4th quarter, we do not believe the market has fully factored in the upside price risk that exists.

Notes:

- The global HRC price was slightly lower and have been down 19 of the last 23 The current spread decreased to $29, the lowest level since February 17th.

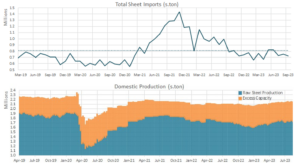

- Our first look at September imports suggests that arrivals remain subdued – mostly likely through the end of the year, given the risk of holding excess inventory in many of the port cities.

- Capacity Utilization fell further last week, down another 2% to 76%. This translates to 1.729M tons per week of raw steel but total capacity available (production + excess) remains elevated. Through the beginning of November, announced maintenance outages will mean that up to 10% of all available production will be offline over the next 9 weeks.