Fundamental Report

Supply-Side Takeaway: The domestic market experienced its first significant production drop; however, despite this encouraging sign, the softer-than-anticipated demand will take time to chew through the surplus. Furthermore, July’s imports are indicating an uptick from June’s easing of arrivals. Thus, in the near term, prices are likely to remain under pressure.

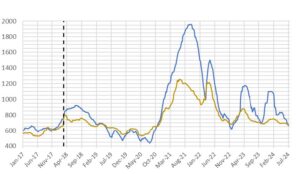

Imports and the Domestic: Global HRC price differential contracted further, continuing to remain negative. This week’s convergence was the result of the domestic spot price dropping further, while the global average experience a slight rise. On the imports side, we received our first look at July arrivals, with preliminary data pointing to a notable increase from June’s import estimate. Given that it is the first week of data for July, we anticipate this figure to be revised, yet maintain to be higher level than June’s ease of imports. Finally, domestic production notably ticked down, falling below the 1.7m net tons level, hitting its lowest level since January.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price rose to $684 from $682. This increase was mainly due to a +$6 in Europe, a +$5 in China, and a +$1 in Korea.

- The Domestic – Global HRC spread contracted further this week, narrowing from -$7 to -$19.

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for July indicate a substantial increase from June’s easing, rising to 1041k tons from June’s estimate figure of 864k.

- Potentially seeing the impact/roll over from the shipping delays as the begin to That said, expect volatility as we move towards the long run average.

Domestic Production (s.ton)

- For the week ending on July 6th, capacity utilization ticked down by -1.2% to 76.3% and domestic raw steel production fell to 1.695m from 1.721m/tpw, its first time below 1.7m since January.

- This brings the year-to-date production to 45.569m, operating at a rate of 4%, -2.7% below this point last year.