Fundamental Report

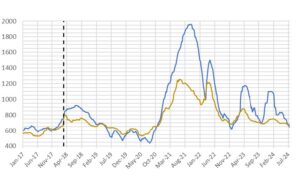

Supply-Side Takeaway: The surplus of material remains intact, while July import expectations were revised lower, to show a more modest uptick from June. The global adjusted HRC spot price reached its lowest level since late 2020. The domestic price continues to slowly approach additional fundamental support levels.

Imports and the Domestic – Global HRC price differential contracted further, reaching its lowest spread since January 2023. This week’s decline was the result of the domestic spot price dropping further than the global average price fell. On the imports side, July arrivals were revised notably lower. However, the estimated level continues to point to an increase from June’s import estimate, which maintains a substantial easing. Finally, domestic production rebounded after briefly dipping below the 1.7m net tons level last week, jumping up to its highest level since the end of May.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price declined to $677 from $684. This drop was mainly due to a -$17 in Russia, a -$10 in China, a -$7 in Korea and Brazil, and a -$6 in Turkey. Europe had the only increase, which was +$4.

- The Domestic – Global HRC spread contracted further this week, narrowing from -$19 to -$27, the lowest since January 2023.

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for July indicate an increase from June’s easing, rising to 897k tons from June’s estimate figure of 865k.

- Potentially seeing the impact/roll over from the shipping delays as the begin to That said, expect volatility as we move towards the long run average.

Domestic Production (s.ton)

- For the week ending on July 13th, capacity utilization surged by 1.8% to 78.1% and domestic raw steel production climbed to 735m from 1.695m/tpw (the highest level in 6-weeks).

- This brings the year-to-date production to 47.304m, operating at a rate of 5%, -2.5% below this point last year.