Fundamental Report

Supply-Side Takeaway:

The global price has seemingly stabilized amid signs of easing import levels and domestic production. Given the upcoming planned outages and our expectation for import levels to continue to decline, the risk remains more skewed to the upside for domestic steel pricing.

Imports and the Domestic – Global HRC price differential was essentially flat as the domestic spot price held steady, while the global average price was relatively unchanged. On the imports side, August arrivals preliminary data this week indicates a decline from July’s rebound, coming in line with our expectations. Finally, domestic production pulled back yet remains on the higher end of the recent range.

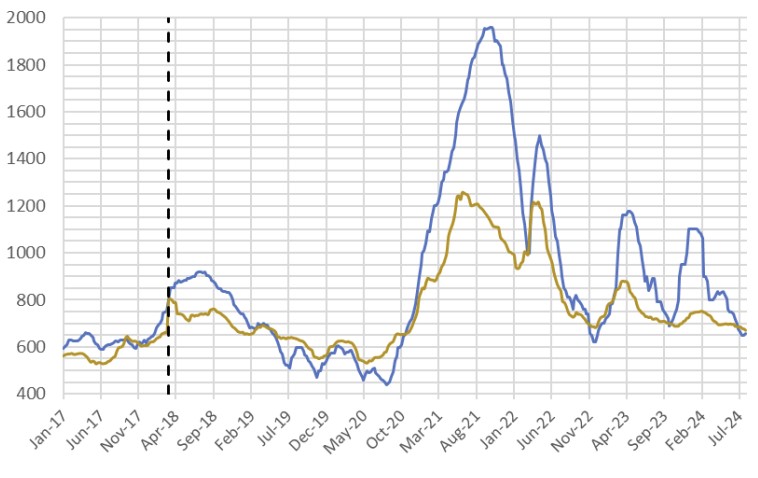

HRC Spot Prices – US Domestic & Global

HRC Spot Prices – US Domestic & Global

- The global HRC spot price was flat again at $652. This week the main movers were China rising by $11 and Europe declining by -$12. Also, Korea rose by $3, while Turkey fell by $3.

- The Domestic – Global HRC spread was also essentially flat, widening from $37.82 to $37.94.

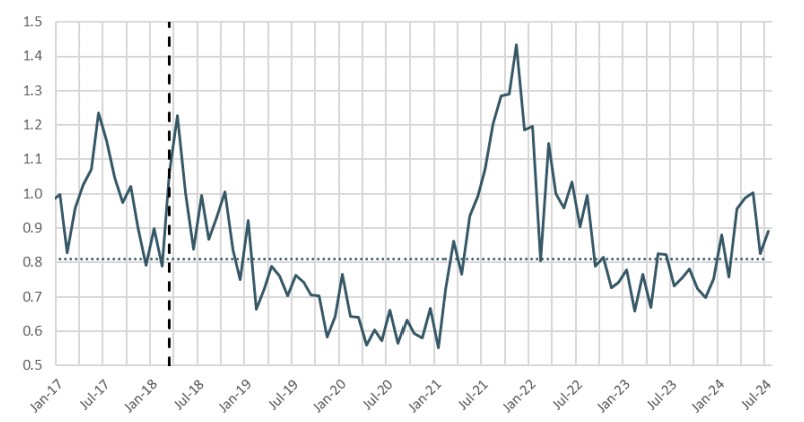

Total Sheet Imports (s.ton)

Total Sheet Imports (s.ton)

- This week’s imports estimated sheet arrivals for August indicate a decline from July’s rebounding, falling to 889k tons from July’s census data figure of 931k.

- Given the current negative differential, it is highly unlikely that we would see another surge in arrivals for the remainder of the year. That said, we do anticipate some volatility in these figures as we push below the longer run “neutral level”.

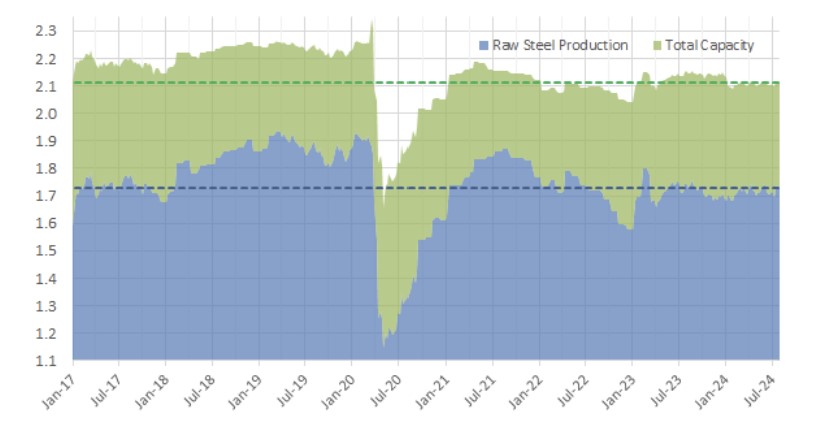

Domestic Production (s.ton)

Domestic Production (s.ton)

- For the week ending on August 31st, capacity utilization ticked down by 1.0% to 79.2% and domestic raw steel production fell to 1.760m from 1.782m/tpw.

- This brings the year-to-date production to 59.338m, operating at a rate of 6%, -2.0% below this point last year.