Fundamental Report

Supply-Side Takeaway:

While headwinds remain in the domestic market, current supply/demand dynamics point to higher domestic steel prices going into the end of the year.

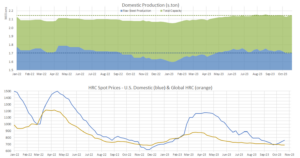

Global production continues to trend lower, driven by cuts coming out of China and domestic raw steel production remains depressed. The Domestic – Global differential expanded further, driven by higher US prices. Global prices showed their first signs of life in 6 weeks, with Europe and China ticking slightly higher.

Notes:

- Global production down 1% MoM, 8.7% below March peak.

- China down 5% MoM, down 2% from March peak.

- RoW ticked higher, driven by increases in EU and the Middle East, up 7%, yet 4.2% below the peak in May .

- Total US domestic capacity available remains elevated, near the August high water However, depressed capacity utilization (up slightly this week) is keeping raw steel production down near late April lows.

- The global HRC price ticked slightly higher, with China and Europe both increasing slightly, while Southeast Asian prices continue to grind lower, offsetting some of those gains.

The domestic – global HRC spread has increase by $80 since briefly turning negative.