Fundamental Report

Supply-Side Takeaway:

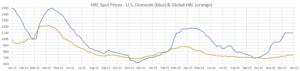

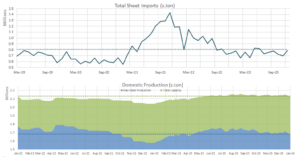

Upward pricing momentum in the US is waning as production scales back capacity further amidst rising imports and global spot prices.

The spread between Domestic – Global prices is narrowing due to global price increases, this week led by Korea’s price jump and China continuing to pick up pace, in contrast to the stagnant domestic spot price. Imports, although revised lower, still reveal a noticeable up- tick from November. Additionally, US domestic production pulled back even further, reflecting efforts to control supply after seeing a substantial gain two-weeks ago.

Notes:

- The global HRC spot price rose to $744.77, with China, Korea, and Europe being the main drivers behind this most recent increase.

- China increased by $5.67 to $642.97, and Korea increased by $9.98 to $544.31.

- The Domestic – Global HRC spread fell to $355, mainly due to the domestic spot price unchanging and the global price slightly rising.

- Imports estimated arrivals for December are 784k, up from November’s estimated arrivals of 689k

- Estimated arrivals for December have been revised lower than the estimates in the beginning of the month, which were in the 800k+ range

- For the week ending on December 29th, capacity utilization ticked down by 6% to 73.1%, bringing domestic raw steel production down to 1.680m net tons.