Macro Deep Dive

Labor Market

Takeaway: The latest labor market data indicates a significant cooling of job market conditions compared to two years ago. The unemployment rate rose to its highest level since November 2021, and job growth has slowed. While wages continue to rise, the pace has slowed, suggesting reduced inflationary pressure. This cooling labor market bolsters expectations that the Federal Reserve may begin cutting rates as early as September. For steel demand, a rate cut could stimulate growth and provide relief. However, ongoing labor market softening could weaken production in steel end-user sectors, as well as potentially hinder demand.

The Unemployment Rate rose to 4.1%, the highest since November 2021, up from 4.0% in May and surpassing expectations to remain unchanged.

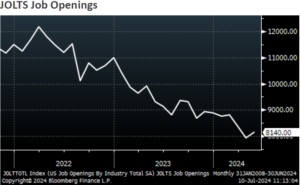

JOLTS Job Openings increased by 221k in May to 8140k, beating the market consensus of 7910k. This follow April’s figure, which was revised down to 7919k, the lowest in three years. Notably, durable goods manufacturing job openings rose by 97k.

Challenger Job Cuts reported 48,786 job cuts in June, a -23.6% decrease from May’s 63,816 but a 19.8% increase year-over-year. This marked the highest June total since 2020, and the highest excluding 2020 since 2009. Notably, Construction had a significant cut of 4,613, a 1,674% increase from May.

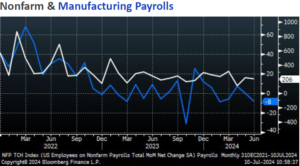

Nonfarm Payrolls added 206k jobs in June, slightly below May’s 218k but above the forecasted 190k. Of note, combined downward revision in May and April resulted in a reduction of 111k jobs. Overall payrolls show signs of cooling as the average monthly payroll growth of 2024 is 222k, down from 251k in 2023 and 377k in 2022. However, a notable gain was seen in construction (27k).

In the last week of June, Initial Jobless Claims rose by 4k to 238k, exceeding the anticipated 235k and staying near the 10-month high of 243k. Continuing Claims increased by 26k to 1858k, the highest level since November 2021. Additionally, the Jobless Claims 4-week Average rose to 238.5k from 236.25k, the highest since August 2023. While these figures are still not drastically high, the upticks suggest cooling in the labor market.

Average Hourly Earnings increased by 0.3% in June, following a 0.4% rise in May and slightly below the projected 0.4% gain. Year- over-year, earnings grew by 3.9%, the smallest annual increase since June 2021.

In the manufacturing sector for June, Manufacturing Payrolls decline by -8k, following a flat reading in May, and contrary to the anticipated 6k rise. Broader manufacturing sector labor market conditions remain soft with weakening labor subcomponents in FED Manufacturing Surveys. The ISM Manufacturing employment index contracted after a brief expansion in May. However, the S&P Global US Manufacturing PMI employment showed the fastest increase since September 2022.