Macro Flash Report

Construction Spending

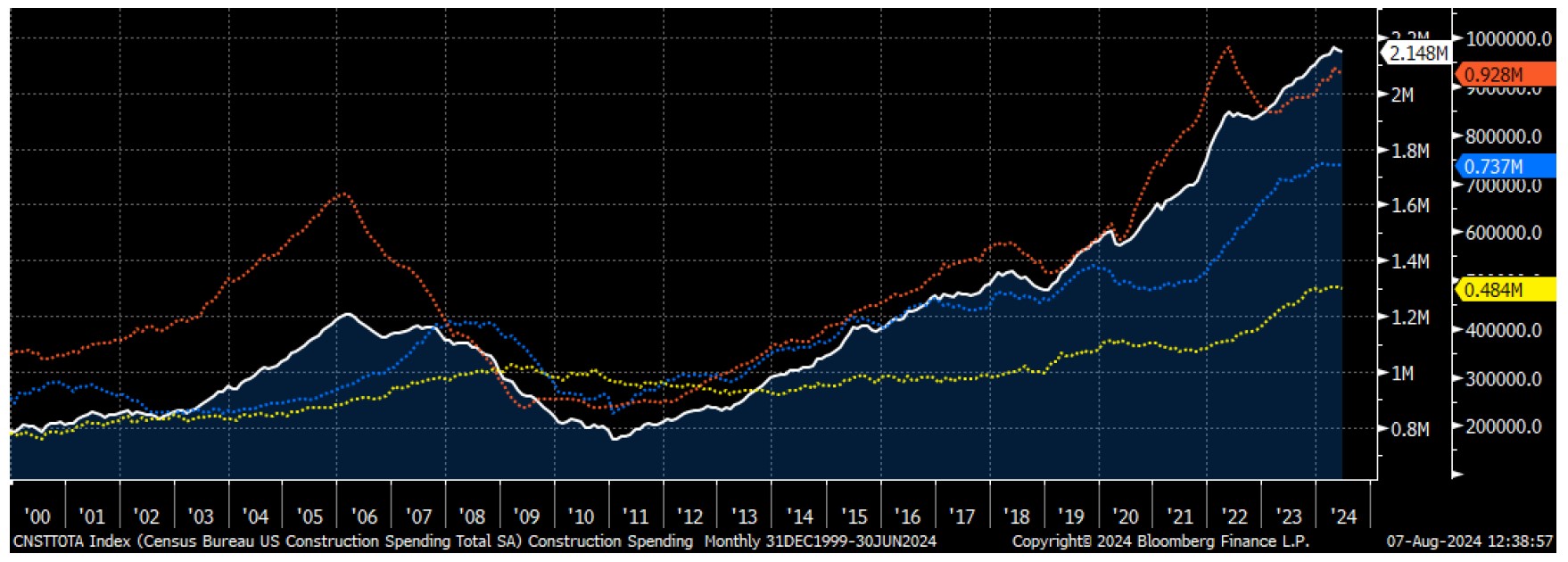

Takeaway:

June construction spending continued to disappoint, coming in below expectations for the 5th month out of the last 6. Looking forward, construction spending was one of the first economic datapoints to feel the negative impact of higher interest rates, now that the cutting cycle is about to begin, we anticipate an improved outlook and activity in short order.

Construction Spending

Total (white) Residential (red) Non-Residential (blue) Public (yellow)

Construction Spending fell by -0.3% to a seasonally adjusted annual rate of $2,148 billion in June, following a revised -0.4% decrease in May, and missing market forecasts of a 0.2% increase. This marks the second consecutive month of declines.

- Private spending fell by -0.3%, with a notable -1.2% drop in single-family residential projects overshadowing a 1% increase in multi-family housing.

- Non-residential spending also dipped slightly by -1%.

- Public construction spending decreased by -4%.

- YoY Total Construction Spending remains positive, up by 2% in June.

The continued decline in construction spending, particularly in the residential sector, signals ongoing challenges in the construction industry, impacting the demand for steel. Reduced activity in single-family projects, while not as significant a factor of steel consumption compared to non-residential projects, suggests that headwinds for bigger projects remain in place and could suppress steel demand in the through the end of the year. Taking a step back, the interest rate cutting cycle is about to begin. It only took 2 months for the negative impact of higher rates to cause residential spending to temporarily peak and roll over, so we anticipate the positive impact on the pipeline to be seen swiftly.