Macro Flash Report

FED MANUFACTURING REPORT

Takeaway:

Overall, the April FED Manufacturing surveys point to continued contraction in the manufacturing sector, although the fundamentals are improving. The ISM Manufacturing PMI surprised to the upside in March, but April is currently expected to print down from 50.3 to 50 (still technically expanding). While there are underlying signs of improvement, we expect the manufacturing sector to tread water over the next 3 months. Therefore, a brief return to contraction territory in April would not be surprising.

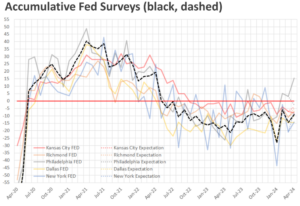

NY Empire showed some recovery, climbing to -14.3 from -20.9, yet fell short of -9.0 expectations, marking the fifth consecutive month in contraction.

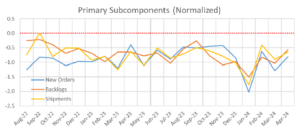

- This move was characterized by new orders (-17.2 to -16.2) and a notable drop in shipments (-6.9 to -14.4), alongside a continued reduction in unfilled orders (-10.9 to -10.1).

- Employment (-7.1 to -5.1) and working hours (-10.4 to -10.6) worsened, input costs rose (28.7 to 7), and selling prices (17.8 to 16.9) remained stable.

- Despite challenges, a modest hopeful outlook persists, with expectations of improvement in the next six months (21.6 to 7).

Philadelphia jumped from 3.2 to 15.5, substantially surpassing forecasts of 1.5. This represents the third consecutive expansionary reading and the highest since April 2022.

- Growth was seen in new orders (5.4 to 2) and shipments (11.4 to 19.1).

- Employment further declined (-9.6 to -10.7), and the price indexes continued to rise, with paid (3.7 to 23) and received (4.6 to 5.5).

- Future activity indicator, though lower, stayed positive (38.6 to 34.3), reflecting expected growth over the next six months.

Dallas slightly dipped to -14.5 from -14.4, and well below the anticipated -11.3, signaling ongoing challenges.

- An improvement was notable in new orders (-11.8 to -5.3), and both shipments (-15.4 to 5) and production (-4.1 to 8) turned positive.

- Employment remained stable (1.5 to -0.1), with wage pressures increasing (20.4 to 30.6) and price pressures easing (11 to 5.5).

- The six-month expectation grew modestly (1.3 to 9), suggesting cautious optimism about future growth.

Kansas City edged down to -8 from -7, underperforming against the expected improvement to -5, indicating a mild worsening.

- New orders (-17 to -6) and backlogs (-27 to -18) grew slightly, while shipments (-5 to -11) and production (-9 to -13) declined.

- Employment (6 to -2) and workweek (-11 to -3), as well as prices received (5 to 0) and paid (17 to 18) were largely unchanged.

- The future composite merely increased (1 to 2), hinting at modest anticipated improvements.

Richmond rose to -7 from -11, beating the forecasted -8.

- There were increases in new orders (-17 to -9) and shipments (-14 to -10), and a reduction in backlogs (-25 to -17).

- Employment saw a slight decline (0 to -2), while price growth rates moderated for paid (3.22 to 2.79) and received (2.23 to 2.37).

- Looking ahead, the outlook improved (12 to 16), as expecting gains in shipments and new orders.