Macro Flash Report

Consumer Price Index (CPI)

Takeaway:

Today’s August CPI came in line with expectations while Core CPI (a measure of underlying price pressure) was slightly higher than expectations. This move will not deter the Fed from cutting interest rates next week; however, it does suggest that a cut larger than 25bps is highly unlikely given this and last week’s “just right” labor market data.

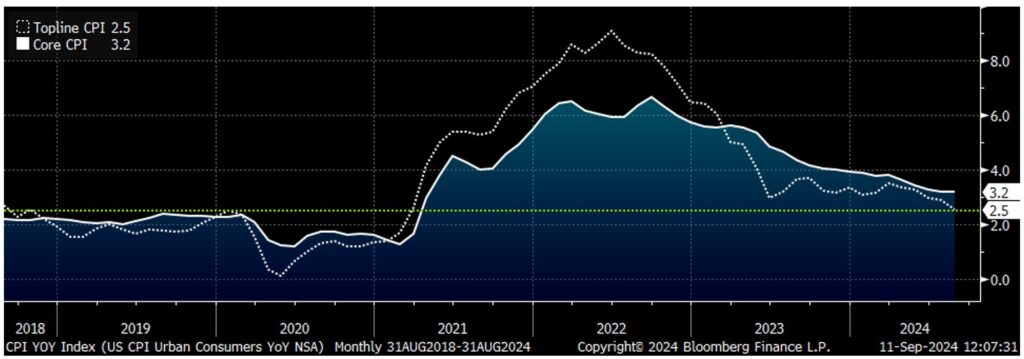

CPI – Topline (dotted), & Core (solid)

In August, Core (Ex Food & Energy) CPI rose by 0.3%, surpassing market expectations of a 0.2% and reflecting a modest gain from July’s 0.2%. This pick up represents the largest monthly increase in four months and has been mainly attributed to shelter as the driving force.

- Shelter (0.5% vs 4%) accelerated for the second consecutive month, reaching the most since the start of the year.

- Transportation services (0.9% vs 4%) was also a contributing factor.

On an annual basis, Core CPI YoY increased by 3.2%, the lowest rate since April 2021, consistent with forecasts and matching July’s pace.

- The shelter index, which climbed 2%, (up from 5.1% in July), accounted for over 70% of the overall rise in the core inflation index.

- Other notable price hikes included motor vehicle insurance (+16.5%), medical care (+3%), recreation (+1.6%), and education (+3.1%).

The overall CPI rose by 0.2% from July and 2.5% year-over-year in August, both aligning with market expectations.

- This marks the fifth consecutive month of easing in the annual measure, largely influenced by declining gas

Looking forward, the NY Fed 1-Year Inflation Expectations in August remained steady at 3%, unchanging from July and June. The 5-Year Inflation Expectations, similarly, held stable, remaining at 2.8%.