Macro Flash Report

Housing Sector

Takeaway:

September housing data started the month with housing starts and building permits down slightly but in line with expectations. Volatility in 30yr fixed mortgages driven by a lack of forward guidance and demand for refinancing will likely keep starts and permits in a tight range through the end of the year.

Housing Starts & Building Permits

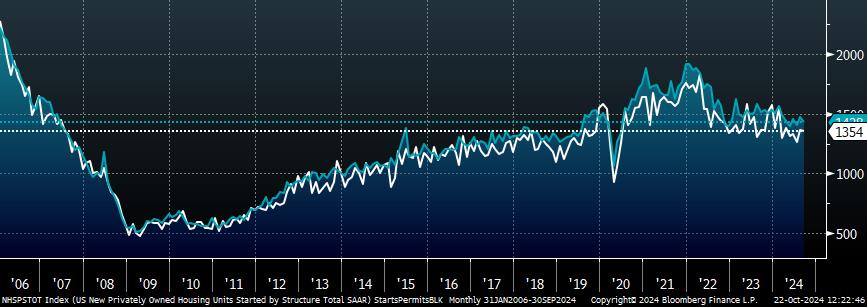

In September, Housing Starts eased by -0.5% month-over month to an annualized rate of 1,354k units, just below the market expected -0.4% drop (1,350k units) and marked a slowdown from August’s 7.8% increase (1,361k).

• The decline was mainly driven by a drop in multifamily projects (-4.5% to 317k), which outweighed a pickup in single-family units (+2.7% to 1,027k), the highest level in five months.

Building Permits, a forward-looking indicator of construction activity, fell by -2.9% in September to an annual rate of 1,428k, below the forecasted decline of -0.7% (1,450k units) and down from August’s 4.6% increase (1,470k).

• A drop in multifamily approvals (-10.8% to 398k) offset a modest gain in single-family authorizations (+0.3% to 970k).

• Of note, the entire “miss” versus expectations can be attributed to a -50k move in the South region.

The NAHB Housing Market Index, which tracks single family homebuilder sentiment, rose to 43 in October, up from 41 and above the anticipated 42. This improvement, the highest since June, was driven by a rise current sales conditions (+2 to 47) and a sharp increase in sales expectations for the next six months (+4 to 57), reflecting optimism that potential rate cuts by the Fed will boost demand.

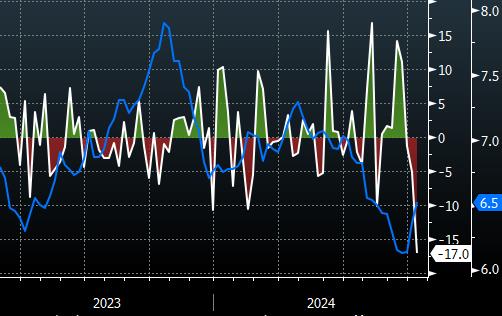

Since September 18th, the day the FOMC cut 50 bps, the long-term Treasury yield has increased more than 50 bps from 3.7% to 4.2% as the labor market shows resilience and inflation remains sticky. In the week ending on October 11th, the MBA 30-Year Mortgage Rate (blue, below) soared to 6.52%, the highest in about two months, and unsurprisingly, MBA Mortgage Applications sank by -17%. Another factor driving mortgage rates higher is heighted demand for refinancing. Ahead of the first rate cut, mortgage rates reached a 2-year low and applications to refinance (white, below) surged in response. Looking at the three most recent spikes in refinancing (chart below) we assume that this increased overall awareness in mortgage rates is driven by demand for refinancing, and it will likely be another factor keeping keep mortgages volatile and elevated until this backlog is worked through.