Macro Flash Report

Fed Manufacturing Surveys

Takeaway:

Overall, the FED manufacturing surveys indicate that the upward trend, which began in July, continued through January. Furthermore, the aggregate number shows that activity in the U.S. manufacturing sector expanded for the first time in 34 months (April 2022).

Aggregate Fed Manufacturing Survey

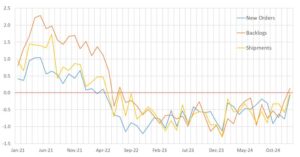

Primary Subcomponents

Richmond improved to -4 in January, surpassing the market expected -13 and up from -10 in the prior month. This marks the mildest contraction since May 2024.

- Support was seen from a slower drop in new orders (-4 vs -11), allowing a slight advancement in shipments (-9 vs – 11).

- Six-month expectations remained rosy (32 vs 40), albeit eased.

Kansas City held steady at -5, missing the forecasted increase to 0. This marks the 17th consecutive month of negative readings.

- Production fell (-9 vs -6) for a third consecutive month to the lowest level since September. Materials inventories experienced a sharp drop (-11 vs 0), while new orders continued to decline, though at a slower pace (-6 vs -16).

- Expectations for activity were slightly less optimistic (15 vs 17) yet remained in expansion.

Philadelphia soared to 44.3 from December’s -10.9, significantly exceeding the anticipated rise to -5. This marks the highest reading since April 2021 and the largest monthly gain since June 2020.

- New orders (42.9 vs -3.6) and shipments (41 vs 1.7) surged, reaching multiyear highs.

- The future activity index also jumped (46.3 vs 33.8), suggesting more widespread expectations for growth.

Dallas advanced to 14.1 in January from December’s 4.5. This represents the second consecutive month in expansionary territory and the highest print since November 2021.

- Production (12.2 vs 5.3) improved to the highest level since October 2021 and new orders (7.7 vs 1.5) hit the highest since April 2022.

- The outlook index (18.7 vs 12.3) and six-month expectations (35.5 vs 20.6) both improved to their highest levels since July 2021.

NY Empire dropped to -12.6 from 2.1 in December, falling short of the expected 3. This marks a return to contraction after two consecutive months in expansion and at the sharpest rate since May 2024.

- New orders (-8.6 vs 4.3) and shipments (-1.7 vs 9.1) both declined back into contractionary territory.

- Despite this, six-month expectations grew more optimistic (36.7 vs 26.9), the highest since December 2021.