Macro Report

Week’s Takeaway:

After recent data started presenting a rosier view on steel specific activity, this week took a turn for the worse. Amid sticky inflation and a stable yet softening labor market, the road to recover on the industrial side continues to be rocky.

Notes:

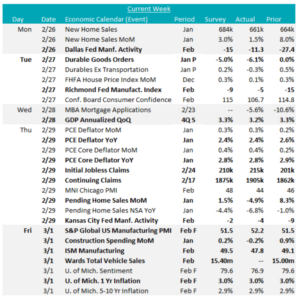

Final February S&P Global US Manufacturing PMI data came in at 52.2 higher than expectations of 51.5, pushing well into expansion territory. However, the more closely watched ISM Manufacturing PMI did the opposite, printing down to 47.8, below expectations of a slight increase to 49.5 The ISM Manu. PMI has now been in contraction territory for 17 months.

Pending Home Sales MoM dropped to -4.9%, a sharp decline from the previous 8.3% rise, and well below expectation of a 1.5% expansion. New Home Sales MoM came in below the forecasted 3.0% and fell to 1.5% growth from the previous month’s revised higher figure of 8.0%.

The PCE Deflator YoY came in at its lowest level since February 2021 at 2.4%, down from 2.6% the month prior, and in line with forecasts. The PCE Core Deflator YoY slightly slowed to 2.8% from December’s 2.9%, the lowest print since March 2021, in line with market expectations.

Construction Spending MoM was down -0.2% in January, it came in below the expected 0.2%, and down from 0.9% in December. This marks the first monthly contraction since December 2022, and was mainly driven by a downturn in public construction outweighing the slight increase in private spending.

The labor market showed a clear signal of softening in this week’s data, with both Initial and continuing jobless claims coming in above expectations. While increasing, initial claims remains well below the threshold which would cause near-term concern for the broader market.

Next Week’s Notes:

Next week’s data will provide insights into durable goods, as well as the labor market.

The final January data for Durable Goods Orders and Durables Ex Transportation will be released, which both surprised to the downside in their preliminary release. However, it is important to note that the substantial slump in former was primarily driven by a downturn in transportation equipment.

For the labor market, we will receive a whole slew of February data. We will the get the weekly update from Initial and Continuing Jobless Claims, as well as Challenger Job Cuts YoY. The Change in Nonfarm Payrolls is forecasted to decline to 190k from 353k, and, similarly, the Change in Manufacturing Payrolls is expected to decrease to 10k from 23k. The Unemployment Rate for has market expectations to stay steady at 3.7%, and the Average Hourly Earnings MoM is anticipated to dip to 0.2% growth from 0.6% the month prior. Overall, these market expectations align with a cooling labor market.