Macro Report

Week’s Takeaway:

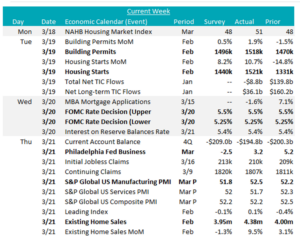

Housing data from this week was strong and manufacturing data highlight the burgeoning recovery. The FOMC held rates steady (as expected) at this week’s meeting but still signal 75 bps of cuts this year.

Notes:

The most important event from the week was Wednesday’s FOMC meeting, where they also provided an update to the SEP (Summary of Economic Projections). Since its last publication in December, the median FED forecast for year-end 2024 points pointed to a stronger U.S. economy across the board:

- Higher expectations for GDP this year (2.1% from 4%)

- Lower expectations for Unemployment (4.0% from1%)

- Higher expectations for PCE Core Inflation (2.6% from4%)

- Still pricing in 3 cuts this year (unchanged)

Our interpretation of this tranche of data is that the FOMC members see the risks to price stability and fully employment as equally balanced – meaning although the last leg of inflation moving down to the 2% target may take longer than initially expected, the risk of high interest rates to the labor market is more significant than the risk of reigniting inflationary pressure. The market and the FED are now in line with three cuts this year (beginning in June). Internally, our view of the risks leads us to believe this will be too soon and too many.

Outside of FED speak, we received the first round of monthly housing data. Building permit beat expectations, rising 1.9% versus an expected 0.5% increase. Housing starts also came in better than expectations, up 10.7% versus 8.2%. Furthermore, the NAHB (Builders) housing market index climbed to 51, surpassing the expected 48 print and reaching its highest level since July of last year. Existing home sales also came in quite strong, increasing 9.5% versus an expected drop, down 1.3%. This is the highest level of existing home sales since February 2023. The combination of the data points to a stable and growing housing market with a solid pipeline for continued activity. One question which remains unclear is how much of this is driven by expectations of the FED beginning a cutting cycle in the next 3 months.

Finally, there was an update to data in the manufacturing sector. First, was the March Philly Fed manufacturing survey, which showed continued (albeit slowing compared to Feb data) expansion in the region printing at

3.2 and beating expectations of a contraction at -2.5. Additionally, the S&P Global manufacturing PMI printed in its 3rd straight month of expansion at 52.5, above expectations at 51.8.

Next Week’s Notes:

Next weeks data will provide insights into the housing and manufacturing sectors, as well as several important economic indicators.

For the housing sector, New Home Sales data for February is anticipated to rise to 675k from 661k the prior month, indicating expectations for further activity in the market. Also, we will get the monthly update from Pending Home Sales NSA YoY.

Two more March Fed Manufacturing Surveys will be published, with Dallas forecasted to slightly decline to -13 from -11.3 and Richmond’s Index, which climbed to -5 in February from -15.

Preliminary February figures for Durable Goods Orders and Durables Ex Transportation are expected to both increase, -6.2% to 1.4% and -0.4% to 0.3%, respectively. These forecasts suggest a significant improvement in transportation, which was a drag on the data in the prior month.

The FED’s preferred inflation data will be released on Friday. February’s PCE Deflator YoY and PCE Core Deflator YoY market expectations indicate a slight ramp up in the former, with 2.4% to 2.5% and an unchanged print at 2.8%, when excluding food and energy. On the consumer side, the University of Michigan consumers surveys final March results will be issued, with the Consumer Sentiment index projected to inch up to 76.6 from 76.5 and the Conf. Board of Consumer Confidence is similarly anticipated for a slight increase, rising to 107 for March from February’s 106.7.

Finally, the GDP Annualized QoQ 4Q T will be reported, with current market expectations for the rate to stay at 3.2%.