Macro Report

Week’s Takeaway:

In a week where there is very little major economic data released, inflation expectations from the University of Michigan Consumer Sentiment Survey will highlight concerns around a troubling trend that is starting to take root with inflation.

Notes:

The University of Michigan Consumer Sentiment Survey is now down for 3 straight months after the May preliminary reading printed at 67.4, well below expectations of a print at 76.2. Looking more closely at the data, the 1yr Inflation Expectations reading of 3.5% versus an expected 3.2% might be the most concerning signal. Taking a step back, it’s important to recognize that consumer expectations surveys are historically not accurate predictors of inflations. That said, the significance of this decoupling in expectations should not be taken lightly and if consumers lose faith that price pressure is moving back to the FED’s target, the FOMC will need to move quickly towards more restrictive policy.

Additionally, Initial jobless claims data printed up to 231k for the week, above expectations of 212k and at their highest level since the August, last year. Continuing claims were up slightly to 1,785k versus expectations of 1,782k. Neither of these figures should sound an alarm – the threshold we are monitoring which would signify a structural problem in the labor market is if the 4-week moving average of initial claims surpasses 260k (currently at 215k).

Next Week’s Notes:

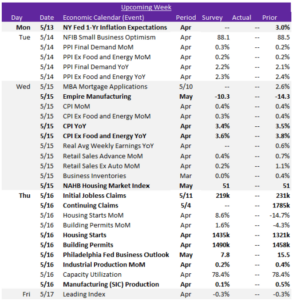

Next week, we will receive some eagerly awaited April inflation data. Market expectations are for a slight decrease in the CPI YoY to 3.4% from the previous month’s 3.5%. Similarly, the CPI (Ex Food & Energy) YoY is projected for a decline to 3.6% from 3.8%. Additionally, the NY Fed 1-Yr Inflation Expectations will be updated, providing further insights into economic outlooks.

In the coming week, we are also set for some key updates from the housing sector. April’s Housing Starts and Building Permits are both anticipated to rise, reaching 1435k from 1321k and to 1490k from 1458k, respectively. For May data, the NAHB Housing Market Index is expected to remain stagnant at 51, indicating stable builder confidence in the market.

Finally, next week will also bring a batch of manufacturing data. The first two May Fed Manufacturing Surveys are set for release, with NY Empire expected to show an improvement to -10.3 from -14.5. Conversely, the Philadelphia index is projected to drop to 7.8 from 15.5, suggesting a cooling, but still expanding, activity. Additionally, April production data will be reported. Industrial Production MoM is forecasted to grow by

0.2%, a slowdown from the prior month’s 0.4% and Manufacturing (SIC) Production is expected for a 0.1% increase, down from last month’s 0.5% growth.