Macro Report

Week’s Takeaway:

This week’s data showed stability in the manufacturing sector, but further disappointed with housing data. Overall economic activity continues to be encouraging and consumers expectations remain buoyant, but volatile.

Notes:

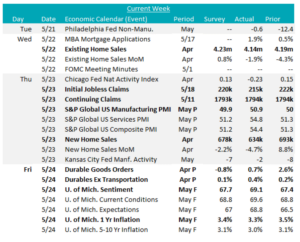

The Kansas City FED Manufacturing survey was up to -2, better than expectations of -7, but the index remains in contraction. Underlying data highlights the fact that a full recovery in the sector will take some time. Additionally, the preliminary May S&P Global Manufacturing PMI beat expectations of 49.9 and rose into expansion territory, to 50.9. This is 5th straight print in expansion territory. April preliminary Durable Goods surprised to the upside as well, with new orders up 0.7%, versus the expected 0.8%. This could also be an encouraging signal for the auto sector which is a major part of this index and has so far disappointed this year.

Housing data came in soft this week, continuing the trend from last week’s starts/permits below expectations. Existing home sales fell by -1.9% to an annual rate of 4.14m units, the lowest level in three months. This compares to an upwardly revised 4.22 million units in March and forecasts of 4.21 million. Similarly, new home sales declined by -4.7% to an annualized 634k, coming in well below projections of 680k. March was also revised down to 665k.

Last, the final May University of Michigan Consumer Sentiment survey data was released and showed that sentiment started improving as the month progressed. The topline index came in at 69.1, above the preliminary reading of 67.4. Both current conditions and expectations improved, but most importantly, the 1yr inflation expectations decreased from 3.5% to 3.3%. While this figure is still trending higher compared to earlier in the year, the severity of concern about prices was reduced.

Next Week’s Notes:

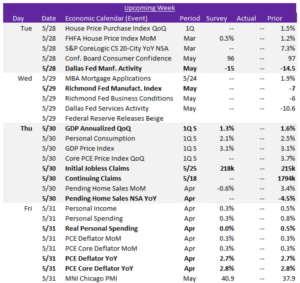

Next week, we’ll receive some sector-specific data, including the final two Fed Manufacturing Surveys for May: the Richmond and Dallas indexes. The Dallas index is expected to drop slightly to -15 from last month’s -14.5. We will also see the release of Pending Home Sales NSA YoY for April.

In additional, a range of macroeconomic data is scheduled to be issued. The GDP Annualized QoQ for 1Q S is forecasted to show a 1.3% increase, down from the previous reading of 1.6%. Furthermore, the highly anticipated PCE data for April will be reported. The PCE Deflator YoY is expected to hold steady at 2.7% and similarly, the PCE Core Deflator YoY is also expected to stay static at 2.8%. Finally, Real Personal Spending for April is anticipated to decline to 0.0% growth from March’s 0.5% increase. Overall, these projections signal expectations for some slight slowing in market activity.