Macro Report

Week’s Takeaway:

This week’s notable industrial data highlighted the headwinds in the housing sector and showed mostly softer readings in manufacturing activity. We also saw how recent trends in inflation data are encouraging and show an opening for the FED cutting rates as early as September.

Notes:

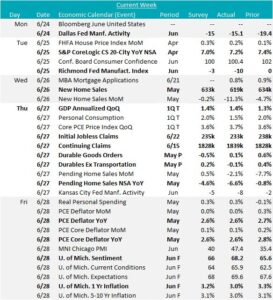

Now that the month is all but over, we have the full set of June FED manufacturing surveys to look for insight into how next week’s ISM Manufacturing PMI may print. Dallas (-15.1, up 4.3 MoM), Richmond (-8, down 6 MoM), and K.C. (-10, down 10 MoM) all remain in contraction with the latter two coming in below expectations and joining Empire (NY) with negative prints. Philly is currently the only regional survey in expansion territory. Taking a broad view of the data, this would suggest next week’s ISM will likely remain in contraction territory for the third straight month, and for 18 of the last 19 months. At the same time, preliminary May Durable Goods New Orders came in better than expectations up 0.1%, versus the expected -0.5%. This was driven by transportation sector, with (ex. Transportation) turning negative, down -0.1%, vs 0.1% expected.

New home sales and pending home sales both disappointed this week on a YoY basis, down 11.3%, and 6.6%, respectively, with affordability noted as a consistent primary concern.

Finally, this week’s Inflation data came with a sigh of relief, as May’s Core PCE YoY (the FED’s preferred reading) printed in line with expectations at 2.6%, down from the April reading of 2.8%. This was also the reading for Topline PCE, down from April’s 2.7% print. Looking more closely, there were two very important signals within the data. First, goods disinflation was strong for the second month in a row, after it had been positive Jan- Mar. Second, this was the lowest MoM reading for Core PCE since November 2020. Furthermore, today’s final June U. of Michigan 1yr Inflation Expectations came in well below the median forecast, and down to 3% (the lowest reading since March).

Next Week’s Notes:

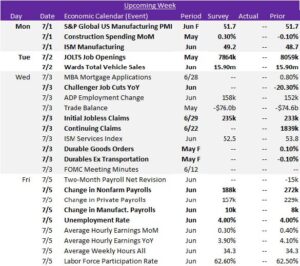

Next week brings a wave of first-of-the-month data releases, providing crucial insights into various sectors and their implications for the steel industry. Starting with manufacturing, the PMIs for June will be reported. The S&P Global US Manufacturing PMI is expected to remain steady at the preliminary reading of 51.7, while the ISM Manufacturing PMI is forecasted to rise to 49.2 from 48.7, which would mark the third consecutive month of contraction despite the slight improvement. These market expectations suggest ongoing challenges, limiting demand for steel, but also potential stability if PMIs hold or improve.

More key data for steel specific sectors will be issued, covering construction, automotive, and durable goods. May’s Construction Spending MoM is anticipated to increase by 0.3%, recovering from the prior month’s -0.1% decline, signaling a boost and potential positive trend for steel demand in construction. In the auto sector, Wards Total Vehicle Sales for June are expected to remain unchanged at 15.90m, indicating stable demand. For Durable Goods Orders, final May data is anticipated, where preliminary results showed a 0.1% increase, marking the fourth consecutive monthly advance. However, Durable Ex Transportation fell by -0.1%, missing forecasts of 0.2% – further highlighting the fact that the auto sector continues to be a key growth driver on the industrial side.

Additionally, a tranche of labor market data, integral for gaining insights into when the Fed may begin cutting rates, will be published. May’s JOLTS Job Openings are expected to drop to 7864k from 8059k, indicating further cooling. The Unemployment Rate for June is forecasted to be unchanged at 4.0%. The Changes in Payrolls are expected to be mixed, with Nonfarm forecast at 188k, down from 272k in May, while Manufacturing Payrolls are expected to increase to 10k from 8k. June data for Challenger Job Cuts YoY and weekly updates for Initial and Continuing Jobless Claims will also be awaited, with Initial projected to rise slightly to 235k from 233k. These market expectations suggest that while conditions remain generally stable, there is added evidence of a softer labor backdrop. This could influence Fed decisions on interest rates and, in turn, affect longer-term investment in steel-intensive projects.

Overall, these indicators suggest a cautiously optimistic outlook for the steel industry, as expectations are for either stability or marginal growth in the steel specific sectors.