Macro Report

Takeaway: This week’s data highlights a modest increase in industrial sector activity, from subdued levels. What does this mean for steel? The biggest risk in the market is the inventory overhang. At these levels of activity resolution of the current surplus could be prolonged.

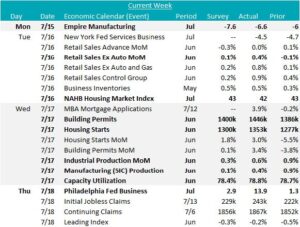

Notes: On the manufacturing side, the first 2 of the 5 monthly FED Manufacturing Surveys for July were released. Empire (NY) printed lower, to -6.6, from -6, but came in above expectations of -7.6. Philly jumped higher, printing at 13.9, up from 1.3 in June, and well above the expectations of a modest increase to 2.9.

Another encouraging datapoint came from June Industrial Production which rose to 0.6% and surpassed the market expectation of a 0.3% print to 104.0 (the second highest reading on record). Capacity Utilization also rose to 78.8%, a 9-month high, while still historically subdued. Looking to the future, the fact that production is so high while capacity utilization is restrained is a very encouraging signal for future steel demand.

Manufacturing (SIC) Production, which accounts for over 75% of industrial production, similarly surprised to the upside, increasing by 0.4% versus the anticipated 0.1%.

On the housing/construction side, Housing Starts and Building Permits both came in above expectations and rebounded from last months local lows. Starts rose by 3% to an annualized rate of 1,353k, above the expectation of a slight increase to 1,300k. Building permits increased by 3.4% to an annual rate of 1,446k, above the expected 1,400k increase. Additionally housing data underscore the current ongoing concerns in the sector, with the NAHB (National Association of Home Builders) Housing Market Index declining for the 3rd straight month in July, printing down 1 point to 42. Like PMI’s, a reading above 50 signals expansion/optimism, while a print below shows contraction/concern.

Finally, Retail Sales from this week highlight the continued divergence between the service and industrial sides of the economy. Topline sales came in at 0.0%, which was better than the expected -0.3% reading. In contrast, Retail Sales ex. Auto came in well above expectations of 0.1%, printing up to 0.4% MoM – the 5th straight month increases. While the auto industry cyber attacks are referenced as culprits for the flat reading, broader data from 1H24 continue to suggest that pent-up auto demand is being kept in check by affordability concerns (i.e. flat production/swelling inventories).

Next Week’s Notes: Next week, we will receive key steel-sector data along with crucial macroeconomic indicators, which will provide insights into the state of these sectors and their implications for the steel industry.

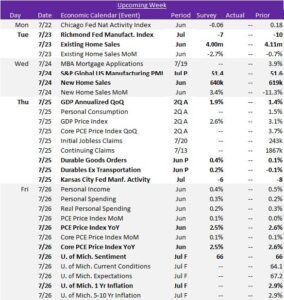

Starting with the manufacturing sector, two more FED Manufacturing Surveys will be released. The Richmond index is expected to climb to -7 from June’s -10 and, similarly, the Kansas City index is projected to improve to -6 from -8. Additionally, preliminary results for July’s S&P Global US Manufacturing PMI are anticipated, with market expectations indicating a slight decline to 51.4 from June’s 51.6. These forecasted figures suggest some improvement and stability, albeit still highlight the ongoing challenges the sector faces, which may hinder steel demand.

Furthermore, in steel specific sector data, preliminary results for June’s Durable Goods Orders will be issued, which is forecasted to increase by 0.4%, up from May’s 0.1% rise. The Durables Ex Transportation is projected for a 0.2% increase, a rebound from May’s -0.1% decrease, suggesting a broader recovery in durable goods beyond transportation, which has been a key growth driver in the recent data.

Finally for steel sector related data, more June housing market data will be published, with Existing Home Sales expected to fall to 4.0m from May’s 4.11m, while New Home Sales is forecasted to rise to 640k from 619k, indicating continued demand.

On the macroeconomic front, the GDP Annualized QoQ for Q2 A is anticipated to increase by 1.9%, a notable uptick from the previous reading of 1.4%. The real time indicator for this datapoint is currently projecting a 2.7% rise, suggesting stronger economic growth, potentially boosting steel demand. In terms of inflation data, the heavily watched and anticipated by the Fed PCE data will be issued. The market expectations are for the PCE Price Index YoY to slightly decline to a 2.5% increase from May’s 2.6% and, similarly, for the Core PCE Price Index YoY to down-tick to a 2.5% rise from May’s 2.6% increase. Also, the University of Michigan consumer surveys final June results will be reported, which are projected to remain in line with the initial readings.