Macro Report

Week’s Takeaway: This week’s data underscore the divergence between the industrial and service sides of the economy. The consumer, labor market, and service sector continue to hold up well (while still cooling), the industrial side fails to break out from the restrained levels of activity.

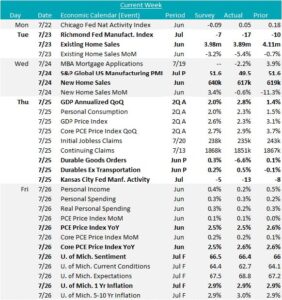

Notes: The most important release from this week was the upside surprise in Q2 GDP, printing up to 2.8%, well above expectations for a slightly rebound to 2.0% and up from the Q1 reading of 1.4%. The only component which was a drag on the economy was net exports which were down 0.7%. Consumption was the primary driver again, up 2.3%, and a continued encouraging signal of overall resilience.

On the industrial side, data was far less rosy. In manufacturing, we saw the S&P Global Manufacturing PMI well below expectations, printing at 49.5, slightly into contraction territory, after expectations were for a flat print at 51.6. Additionally, both the K.C. and Richmond Fed Manufacturing Surveys came in well below expectations, also printing lower MoM, at -13 versus expected -5, and -17 versus expected -7, respectively. Finally, the preliminary topline Durable Goods New Orders data showed the steepest MoM decline since the pandemic, down 6.6% and well below the expected 0.3% rise. Taking a step back, (ex. Transportation) data, suggests this is a transportation issue, as underlying orders have been mostly improving since January.

On the housing front, June’s New Home and Existing Home Sales both disappointed as well. New printed -0.6% versus an expected increase of 3.4%, and existing came in at -5.4% versus an expected -3.2%, respectively. Low overall inventories and affordability concerns continued to negatively impact this sector.

On the inflation side, Core PCE, the FED’s preferred gauge came in slightly higher than expected, up 0.2% MoM, resulting in a flat YoY reading at 2.6%, versus the expected 2.5%. Along with anchored U. of Mich. 1yr Inflation Expectations at 2.9%, the window for a cutting cycle appears to be broadening.

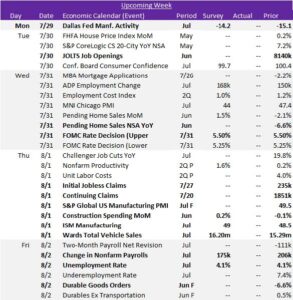

Next Week’s Notes: Next week will be important on the data front as we receive the final releases for July alongside the beginning-of-the-month data, offering significant insights into the steel sector and the labor market, as well as featuring a FED interest rate decision.

Starting with the manufacturing sector, the final July FED Manufacturing Survey and the July PMIs will be released. The Dallas index has market expectations of rising to -14.2 from June’s -15.1. The ISM Manufacturing PMI is forecasted to improve slightly to 49 from June’s 48.5, and the final results of the S&P Global US Manufacturing PMI will be issued, with the preliminary reading at 49.5.

Additionally, June’s Construction Spending MoM is anticipated for a 0.2% increase, a rebound from May’s -0.1% decline, and we will also receive the final June data for Durable Goods Orders, which in initial results sharply disappointed. Furthermore, July’s Wards Total Vehicle Sales are projected to jump up to 16.20m, which would be a notable increase from June’s 15.29m sales.

In the upcoming week we are also set for housing sector data, with updates on prices and rates, as well as June Pending Home Sales.

The labor market will be under scrutiny with the release of fresh data. July’s Change in Manufacturing and Nonfarm Payrolls are expected, with Nonfarm Payrolls anticipated to decline to 175k from 206k. The Unemployment Rate is forecasted to hold steady at 4.1% in July. The additional data will include June’s JOLTS Job Openings, July’s Challenger Job Cuts, the weekly Initial and Continuing Jobless Claims, and updates on wages and labor costs.

Finally, the FOMC Rate Decision will be closely watched. The upper and lower bounds of the interest rate are anticipated to remain unchanged at 5.50% and 5.25%. The market is currently pricing in the first FED Funds cut in September, so the tone of the Chairman will be crucial for providing insights on monetary policy and economic conditions moving forward.