Macro Report

Week’s Takeaway

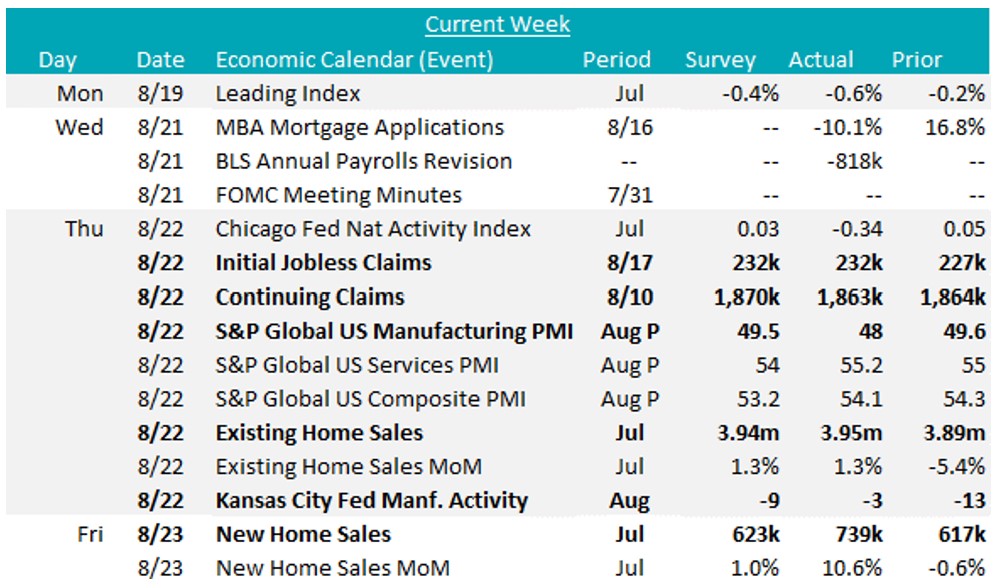

This week’s data show further softness in industrials, while the labor market and services remain stable. The most important signal came from Jackson Hole, WY this morning, when FED Chair Powell, clearly opened the door for the cutting cycle – the ‘time has come’.

Notes:

The August Kansas City Fed Manufacturing Survey printed up to -3, from July’s -13 level, also above expectations of a -9 print. Furthermore, August’s preliminary S&P Global US Manufacturing PMI dropped to 48 in August, down from 49.5 in July and the expected flat print at 49.5. This marks the second straight month in contraction territory, while the Services PMI edged up to 55.2, above last month’s 55 print and expectations of a decline to 54. As has been the case for more than a year – services continue to drive overall economic growth, as industrials face strong headwinds.

The next batch of housing data signaled signs of life, as falling mortgage rates work their way through the system. Existing and New home sales both increased in July, existing sales were in line with the expected 1.3% monthly increase, while new sales rose 10.6% vs. expected 1%. Given the fact that mortgage rates only started to fall at the very end of July, this is an encouraging signal for underlying demand.

Another notable datapoint from this week was the BLS preliminary annual payrolls benchmark revision which suggested that payroll growth was overstated by -818k in the March 2023 to March 2024 period. For months, this was anticipated, with forecasts for the revision coming in at a wide range of 400k-1.1m. This tells us that the labor market grew at a monthly pace of 174k versus the previously assumed 242k. Given the fact that the replacement rate for hiring is ~100k given U.S. demographics, this simply provides that context that the labor market was “strong” rather than “on fire” over the period. Additional labor market data show initial and continuing jobless claims remain at elevated but healthy levels. Initial claims were up slightly to 232k from 227k, while continuing claims decreased to 1,863k from 1,864k. Overall, the labor market should continue cooling in the coming months and the rate at which it does will be instrumental for how the FED determines the pace of the interest rate cutting cycle.

Next Week’s Notes:

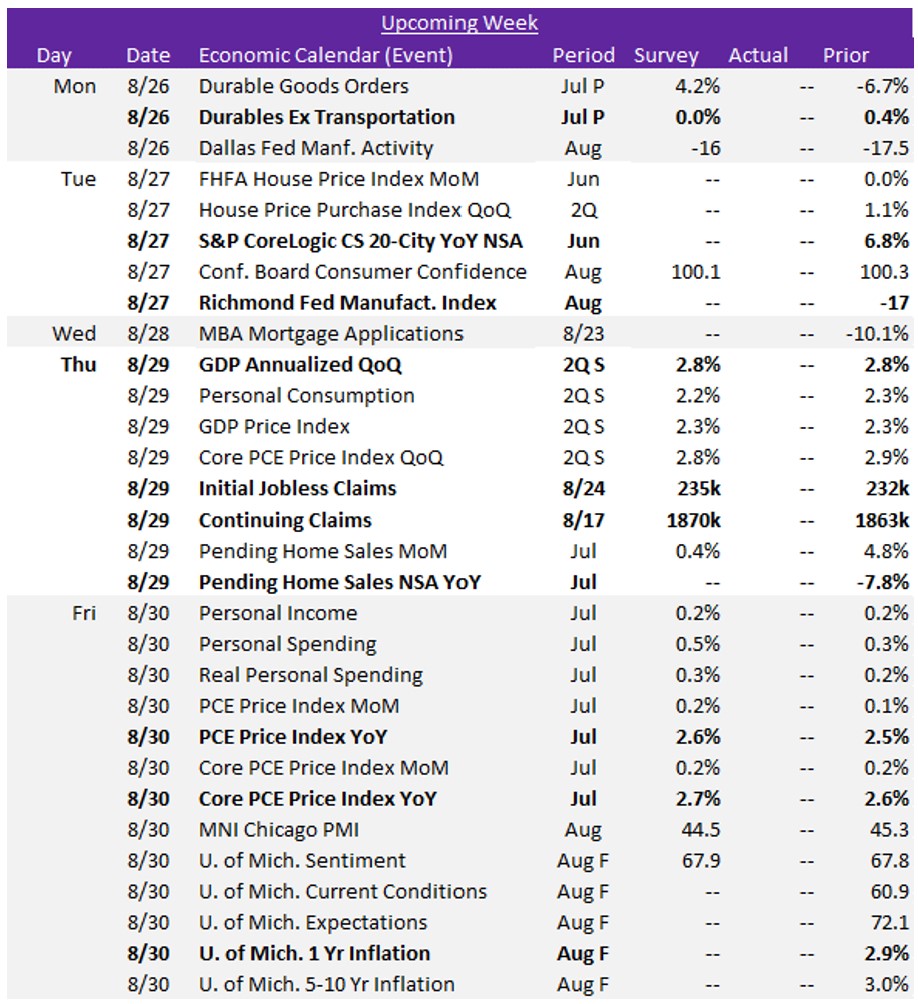

Next week, a range of macroeconomic and steel sector specific data will be released, offering valuable insights into the state of the economy and the steel industry.

Key industrial data includes the release of the Richmond FED Manufacturing Survey for August, the fourth out of five for this month. We will also see the preliminary results for July’s Durable Goods Orders, which are expected to rise by 4.2%, a sharp rebound from June’s -6.7% decline. However, Durables Ex Transportation is forecasted to be flat at 0.0%, down from June’s 0.4% increase, suggesting that the transportation sector is likely to be the primary driver of growth for the month after disappointing in the prior month.

In the housing sector, data on July’s Pending Home Sales YoY and a variety of housing price indicators – including the S&P CoreLogic Case-Shiller 20- City index for June, the FHFA House Price Index for June, and the Q2 House Price Purchase Index – will be issued, proving insights into the ongoing affordability challenges.

On the macroeconomic front, Q2 GDP is expected to maintain a 2.8% annualized growth rate. The Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) Price Index, is projected to show slight up ticks, with the PCE YoY rate rising to 2.6% in July from 2.5%, and Core (Ex Food & Energy) PCE YoY moving up to 2.7% from 2.6%. Additionally, the final results of the University of Michigan’s August consumer surveys will be reported, with the preliminary 1-Yr Inflation Expectations at 2.9%. Also, the weekly Initial and Continuing Jobless Claims are both anticipated to rise slightly, to 235k and 1870k, respectively.