Macro Report

Week’s Takeaway:

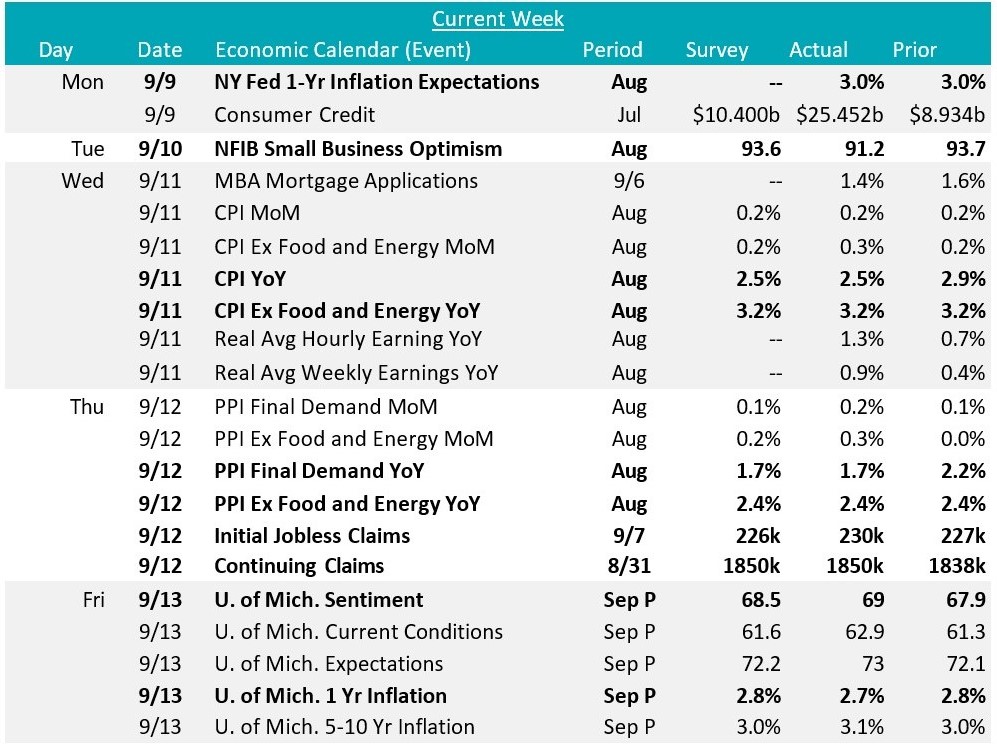

This week was chalk full of inflation data, which cemented expectations of a 25-basis point rate cut by the Fed next week.

Notes:

In August, the Core CPI and overall CPI both met expectations, holding steady at 3.2% and 2.5% YoY, respectively. However, producer price data was slightly below forecasts: the Core PPI came in at 2.4% YoY, versus an expected 2.5%, and the overall PPI was 1.7% YoY, below the anticipated 1.8%. For inflation expectations, the NY Fed’s 1-Year Inflation Expectations remained steady at 3.0%, while the University of Michigan’s 1-Year Inflation Expectations decreased to 2.7%, falling short of the 2.8% forecast.

Additionally, August’s NFIB Small Business Optimism Index dropped to 91.2, missing the expected slight decline to 93.6, likely reflecting ongoing uncertainty related to the upcoming election.

Next Week’s Notes:

Next week will feature key data releases on manufacturing, housing, and a highly anticipated Federal Reserve rate decision.

First, we will receive the September FED Manufacturing Surveys. The NY Empire Index is expected to improve slightly to -4.3 from -4.7, while the Philadelphia Index is projected to rise to -1 from August’s -7. Additionally, Industrial Production for August is forecasted to increase by 0.2%, reversing July’s -0.6% decline, with Capacity Utilization expected to edge up to 77.9% from 77.8%. Manufacturing (SIC) Production is also anticipated to grow by 0.2% in August, compared to a -0.3% decline in July.

In the housing sector, the NAHB Housing Market Index for September is expected to rise to 40 from 39. Housing Starts and Building Permits are both anticipated to rebound, with starts projected to reach 1320k from 1238k and permits expected to rise to 1413k from 1396k. However, Existing Home Sales for August are forecasted to decline slightly to 3.90 million from 3.95 million.

Finally, the Federal Reserve is anticipated to announce a 25-basis point rate cut.