Macro Report

Week’s Takeaway:

This week’s data highlight soft activity in manufacturing and a standoff in housing. Most importantly, inflation data came in better than expected, providing further support for the interest rate cutting cycle to begin shortly.

Notes:

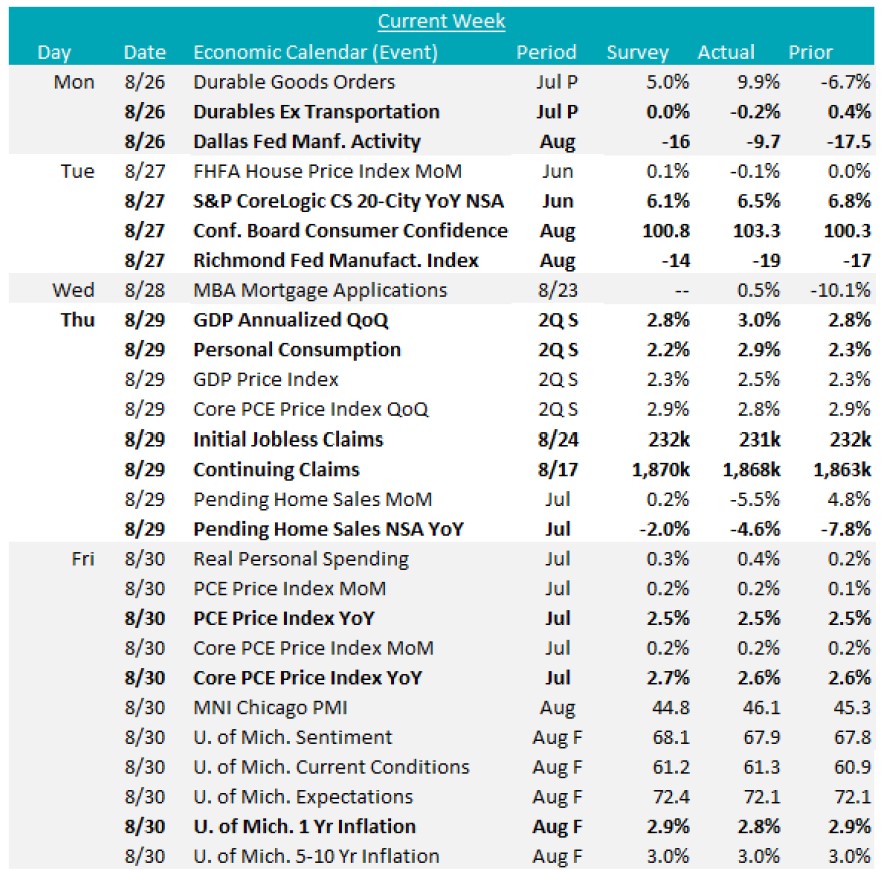

The last of the August FED Manufacturing Surveys were released this week and paint a picture of suppressed activity overall and suggest that we will not see a rebound into expansion for Tuesday’s ISM Manufacturing PMI. The individual readings are below:

- Empire (NY) rose to -4.7, from -6.6 in July, above expectations of –

- Philadelphia fell sharply to -7 from July’s 9, below the anticipated 7.

- Kansas City rose to -3, up from -13 in July, above expected –

- Dallas improved to -9.7, from -17.5 in July, above expected –

- Richmond fell to -19, from -17 in July, below expected –

*While some survey regions improved, all of them are in contraction territory for the first time since February.

July Durable Goods New Orders show a rebound in transportation with topline orders increasing by 9.9%, after a revised -6.9% decline in June. The Ex. Transportation data declined by -0.2%, a shift from the 0.1% growth seen in June and missing the forecasted flat reading.

Pending Home Sales NSA YoY fell -4.6%, below expectations of -2%, to 70.2 in July, the lowest data on record, going back to 2001. The index has been grinding lower since January 2023, with affordability and low inventory as serious hurdles for the housing since the hiking cycle began. In the coming months underlying dynamics in the housing sector are poised to change, with mortgage rates already starting to decline ahead of FED cuts.

The second revision for Q2 2024 GDP increased to 3%, from 2.8%, and underscores stable consumption (up to 2.9%, from 2.3%) as the primary driver of economic growth, while all other components were revised lower.

Topline & Core PCE (Personal Consumption Expenditures) came in line with expectations, with YoY readings for both unchanged compared to June, at 2.5% and 2.6%, respectively. Additionally, the U. of Michigan 1yr Inflation Expectations down to 2.8%, the lowest level since December 2020.

Next Week’s Notes:

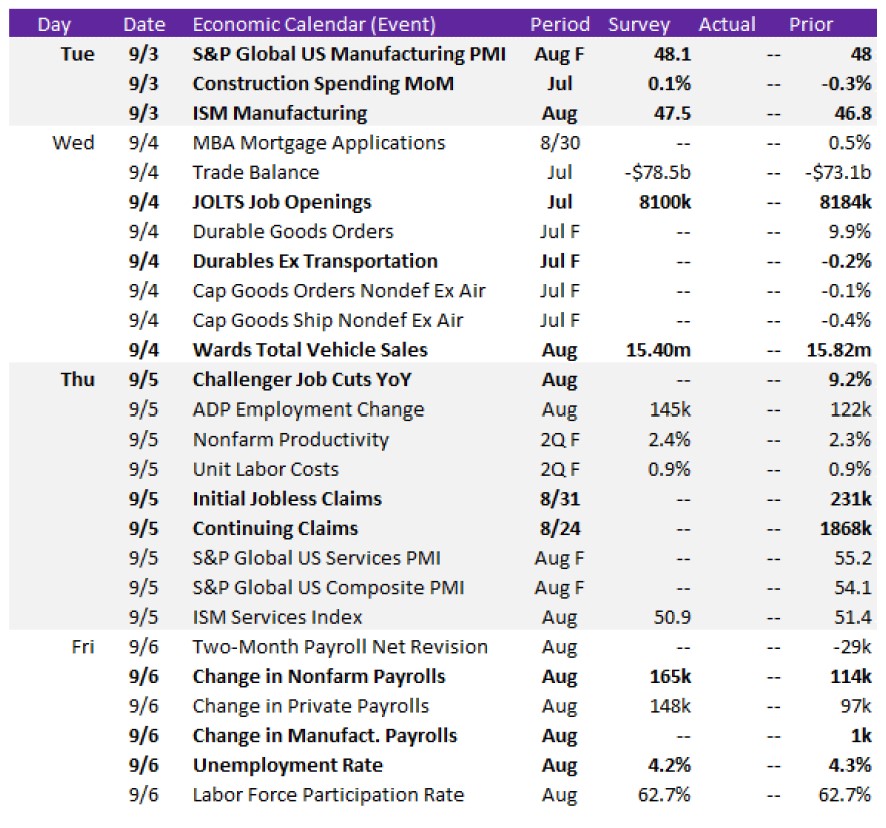

Next week will deliver the first-of-the-month data, providing insights into both steel demand and the labor market outlook.

We will see the final August results for the S&P Global US Manufacturing PMI, which is expected to tick up to 48.1 from the initial 48, and the August ISM Manufacturing PMI, anticipated to increase to 47.5 from 46.8.

Additionally on the industrial front, July’s Construction Spending is forecasted to increase by 0.1%, a rebound from June’s -0.3% decline. The final results for July’s Durable Goods Orders will also be released, alongside Wards Total Vehicle Sales for August, which have expectations to decline to 15.40m from 15.82m.

For labor market data, the JOLTS Job Openings for July are projected to experience a slight decrease to 8100k from 8184k. We’ll also receive August’s Challenger Job Cuts YoY figures, along with the weekly updates on Initial and Continuing Jobless Claims. Furthermore, the Unemployment Rate for August is anticipated to fall to 4.2% from 4.3%, and the Change in Nonfarm Payrolls is expected to rise to 165k from 114k.