Macro Report

Week’s Takeaway:

This week, the FED began the rate cutting cycle with a 50bps reduction, and industrials and housing data showed early signs of improvement. Over the last couple of months, business surveys have long bemoaned elevated borrowing costs and election uncertainty as significant headwinds – after this week, it appears that the former will be alleviated faster than previously expected.

Notes:

The FOMC (Federal Open Market Committee) met this week and announced a 50bps cut to the Federal Funds Rate, bringing the range down to 4.75-5%. The market was more divided than usual heading into a rate decision with 70% pricing in the likelihood of the jumbo cut versus 25bps. The much- watched dot plots also showed an abrupt turn and far more dovish outlook than their last release in June. Previously, the SEP (Summary of Economic Projections) showed a total of 25bps cuts in 2024, but Wednesday’s release showed a total of 100bps (suggesting an additional 50bps over the remaining meeting in November and December). Furthermore, the median dot also shows an additional 100bps in 2025, and another 50bps at some point in 2026. The FED has clearly signaled to the market that their concerns around inflation have fully subsided and they are now focused on keeping the labor market supported.

August housing starts and building permits rose 9.6%, and 4.9%, respectively, both beating expectations of more moderate increases. This was a promising signal ahead of the rate cut, as this sector is clearly the most interest rate sensitive. Existing home sales side, on the other hand, came in at -2.5%, below the expected decline of -1.3%. Under the surface, the 30yr Fixed mortgage led the Fed decision and should support the market ahead, with the national average printing down to a 2-year low, this week.

The industrial side also pro showed further signs of life. The August Empire (NY) and Philly FED manufacturing surveys both came in above expectations at 11.5 v expected -4, and 1.7 v expected 0. Furthermore, Industrial production jumped 0.8%, largely driven by a surge in manufacturing production, up 0.9%. Capacity utilization also improved to 78%, increasing by 0.6% from July.

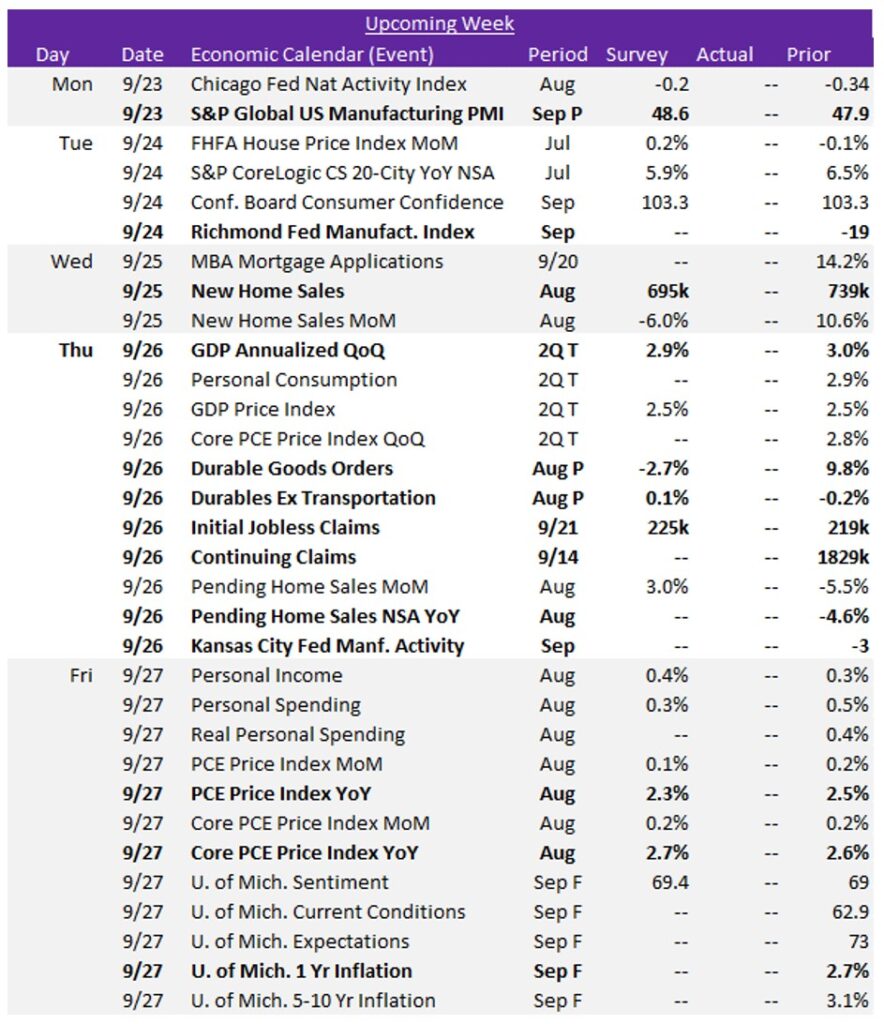

Next Week’s Notes:

Next week, key manufacturing and housing data, along with important macroeconomic indicators, will be released. Market expectations for these sectors suggest some ongoing challenges, while the macroeconomic indicators forecasts indicate more of a mixed landscape, which will influence the overall outlook.

For manufacturing, we will receive two more September FED Manufacturing Surveys: The Richmond Index and the Kansas City Index. Additionally, the preliminary September results for the S&P Global US Manufacturing PMI has market expectations of rising to 48.6 from 47.9. The preliminary August data for Durable Goods Orders is forecasted to decline by -2.7%, a notable drop from the previous month’s 9.8% increase, signaling weakened activity. In contrast, Durables Ex Transportation is anticipated to see a modest 0.1% increase, recovering from July’s -0.2% drop.

The housing market data will also be crucial for evaluating ongoing pressures and insights into buyer sentiment. New Home Sales for August is projected to fall to 695k from 739k, and the August reports on Pending Home Sales will be issued.

On the macroeconomic front, the GDP Annualized QoQ for Q2 is expected to show a 2.9% increase, indicating stable growth, though down slightly from the previous 3.0%, which may signal moderating economic momentum. The highly anticipated PCE Price Index, a key inflation measure for the Fed, is forecasted to decrease to 2.3% YoY in August from 2.5%, suggesting easing inflationary pressures. Meanwhile, the Core PCE Price Index YoY is projected to rise slightly to 2.7% from 2.6%, reflecting ongoing inflation concerns, albeit at a manageable level. Finally, the final September results from the University of Michigan consumer surveys will be released, and Initial Jobless Claims are anticipated to increase slightly to 225k from 219k, indicating further softening.