Macro Report

Week’s Takeaway:

This week’s data underscore a resilient labor market, and slightly improvements on the industrial side. Consumer expectations meaningfully improved, especially around inflation, while the FED cut interest rates by 25bps.

Notes:

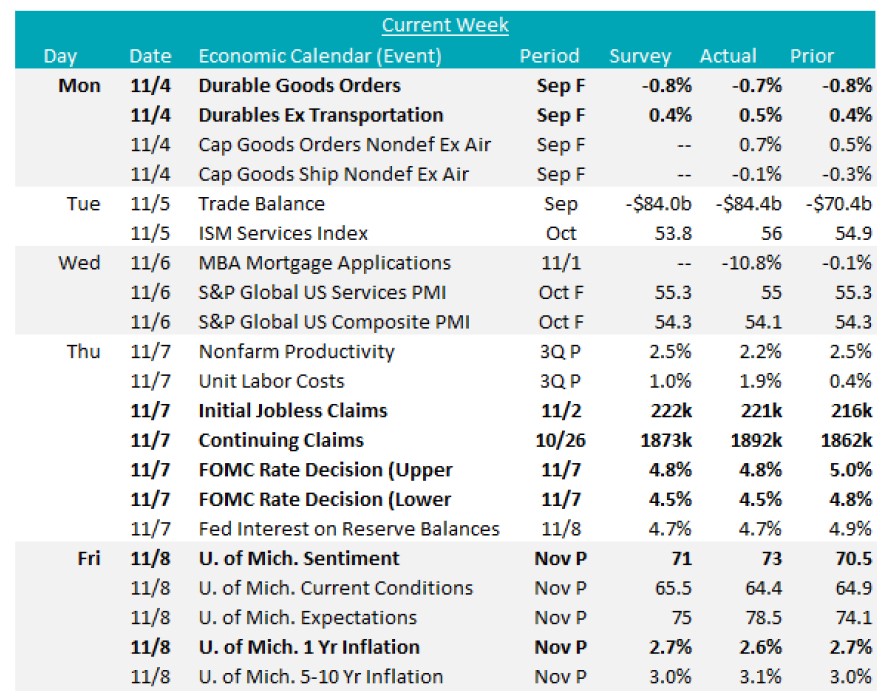

The final results for September’s Durable Goods Orders exceeded expectations, declining by -0.7% versus -0.8%, and up from August’s -0.8% fall. Similarly, Durables Ex Transportation rose by 0.5% versus the 0.4% forecast, improving from August’s 0.4% gain. Together, these suggest that the transportation sector remains weak, with decline in three of the last four months. A key highlight was the 0.7% increase in Orders for Nondefense Capital Goods Ex Aircraft, a leading indicator of business investment plans, following a 0.5% jump in August. This sustained growth reflects optimism and could create a more stable foundation for future steel demand.

Initial Jobless Claims were slightly below market expectations, 221k vs 222k, but up from the prior week’s 216k. Despite this increase, the figure is significantly lower than the averages from earlier in the month, indicating ongoing resilience in the labor market. Conversely, Continuing Claims rose to 1892k, the highest level since November 2021, surpassing the anticipated climb to 1873k from 1862k in the previous week.

Preliminary estimates for November’s University of Michigan consumer surveys, which do not capture any reactions from the election results, showed the Sentiment Index rising to 73, marking the highest level in seven months, up from 70.5 in October and beating the forecasted 71. Additionally, the 1-Yr Inflation Expectation ticked down to 2.6% versus the expectation to hold steady at 2.7%, hitting the lowest rate since December 2020.

The Federal Open Market Committee (FOMC) unanimously voted for a 25bps interest rate cut, bringing down the range of FED Funds down to 4.5- 4.75% from 4.75-5%. The committee noted in the statement that they view risks to the labor market and inflation as “roughly in balance.” While the cutting cycle will continue, Chair Powell also noted that economic data has come in better than expectations of late, suggesting that they may not be as aggressive as the market anticipated a few weeks ago.

Next Week’s Notes:

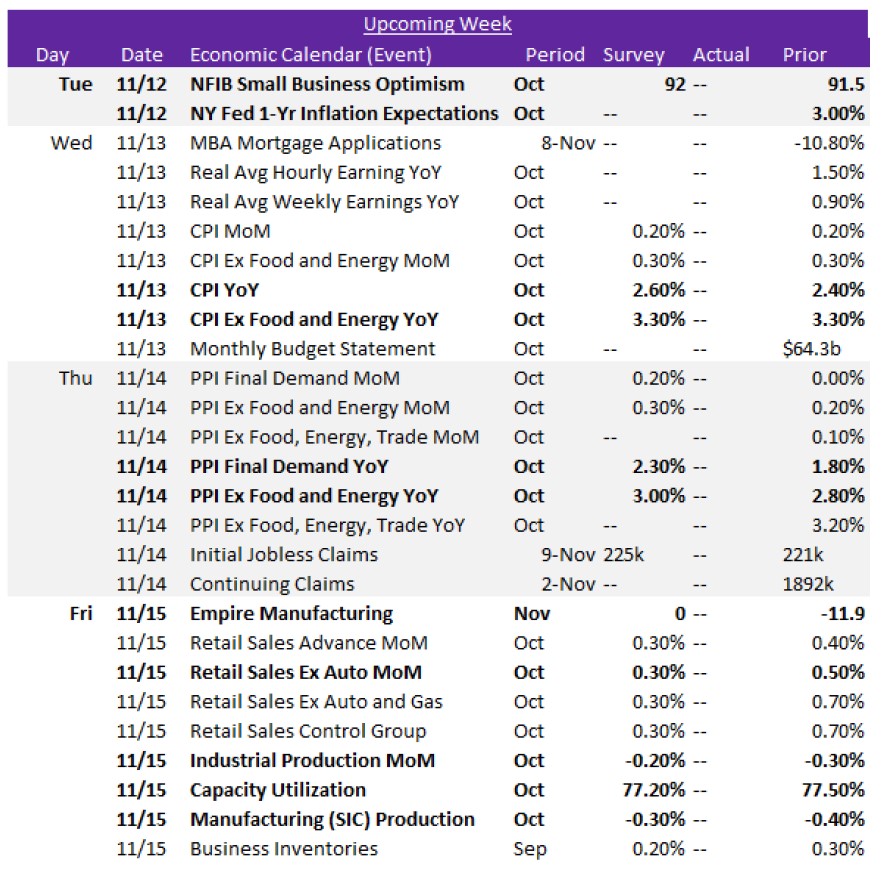

Next week, we will receive key manufacturing data and macroeconomic indicators that will shed light on demand and the overall state of the economy.

In the manufacturing sector, the first of five November Fed Manufacturing Surveys, the NY Empire index, is expected to improve to 0 from -11.9. The October Industrial Production report will also be released, with forecasts indicating a month-over-month decline of -0.2%, a slight improvement from September’s -0.3%. Capacity Utilization is anticipated to operate at a rate of 77.2%, down from 77.5% in the previous month. The report will include Manufacturing (SIC) Production, which is expected to show a smaller decline of -0.3%, improving from September’s -0.4%. Additionally, Retail Sales Ex Auto for October is projected to increase by 0.3%, down from a 0.5% rise in September.

On the macroeconomic data front, several inflation metrics will be released. The Consumer Price Index (CPI) YoY is expected to rise to 2.6% in October from 2.4% in September, while Core CPI (Ex Food & Energy) is anticipated to remain steady at 3.3%. The Producer Price Index (PPI) YoY is forecasted to increase to 2.3% from 1.8% in September, with Core PPI expected to tick up to 3% from 2.8%. Additionally, the NY Fed’s 1-Year Inflation Expectations for October will be reported, along with the NFIB Small Business Optimism Index, which is projected to rise to 92 from 91.5.