Macro Report

Week’s Takeaway:

This week’s data showed near-universal growth in industrial data. Furthermore, the labor market rebounded impressively after hurricanes hampered last months data.

Notes:

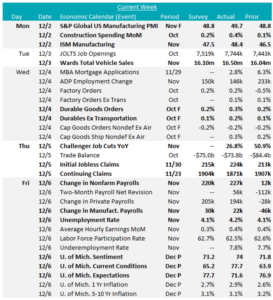

Manufacturing data showed positive momentum this week. Both November Manufacturing PMIs exceeded market expectations, rising to near stabilization in the sector: S&P Global US Manufacturing PMI jumped to 49.7 vs the preliminary 48.8 and ISM Manufacturing PMI surged to 48.4 vs the anticipated 47.5. Notably, growth in new orders was the main driver for these increases. Additionally, October’s Durable Goods Orders outperformed forecasts, increasing by 0.3% compared to 0.2%, with Durables Ex Transportation also rising by 0.2%, surpassing the anticipated 0.1%.

More key steel-consuming sectors saw upside surprises. Construction Spending in October rose by 0.4% compared to the expected 0.2% increase, with private spending leading the growth (up 0.7%), driven by a 1.5% advance in the residential segment. For the auto sector, Wards Total Vehicle Sales soared to 16.50m in November vs the projected 16.10m, the highest since May 2021.

November’s Change in Nonfarm Payrolls came in just above expectations, a clear signal that the concerns floated in last month’s print were in fact driven by hurricanes and labor disputes. The Unemployment Rate increased to 4.2% this month as well, as the labor force expanded. Initial jobless claims came in slightly higher than expected but remains subdued, and continuing claims decreased.

Finally, the preliminary December University of Michigan Consumer Sentiment survey provided fascinating insight into how consumers at large view economic conditions, however it will take months for post election volatility to work its way out. The clearest signal at this point, appears to be slightly elevated inflation expectations, while topline sentiment reached an 8-month high.

Next Week’s Notes:

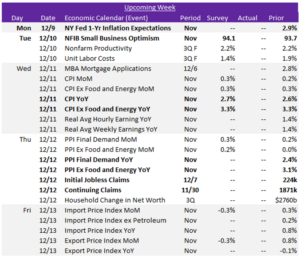

Next week, we will gain insights into sentiment and inflation, providing a clearer picture of economic conditions.

For sentiment, the November NFIB Small Business Optimism index has market expectations of a rise to 94.1 from 93.7 in October, which would be the highest level since February 2022. This signals growing confidence which could support demand for steel. Additionally, the NY Fed 1-Yr Inflation Expectations for November will be released.

On the inflation front, the Consumer Price Index (CPI) report is anticipated to show a slight increase in CPI YoY to 2.7% from 2.6%, while Core (Ex Food & Energy) CPI YoY is forecasted to remain steady at 3.3%. These market expectations suggest stable to slight inflationary pressures. The Producer Price Index (PPI) will also be reported.

Finally, we will receive the weekly updates on Initial and Continuing Jobless Claims.