Macro Report

Week’s Takeaway:

The holiday week’s industrial data came in mixed but provided additional bright spots for a manufacturing recovery early next year.

Notes:

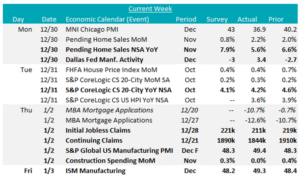

As mentioned above, December manufacturing data from both the S&P Global and ISM Manufacturing PMIs came in above expectations rising to (49.4 vs expected 48.3) and (49.3 vs expected 48.2), respectively. The real reason for optimism when looking at these still contractionary prints comes from the subcomponents. The ISM New Orders index came in at 52.5, up 2.1 points from Novembers print which was also slightly expansionary. Furthermore, the Dallas Fed Manufacturing Index showed an expansion of activity in the region, printing up to 3.4, and beating expectations of a -3 print.

Limited housing data showed softer activity in December with NSA Pending Home Sales increasing 5.6% YoY versus an expected 7.9% increase, while MBA Mortgage Applications showed to consecutive weeks of double-digit percentage declines (seasonally normal around the holidays). Affordability continues to be a concern, with lagged October S&P CoreLogic 20-City YoY house prices cooling less than the expected 4.1%, still up 4.2%.

Jobless claims continue to show a stable labor market, with Initial claims at 211k, their lowest level since March, and continuing claims falling more than expected to 1.84M.

Next Week’s Notes:

Next week we will receive sector-specific data, along with the jobs report and sentiment indicators.

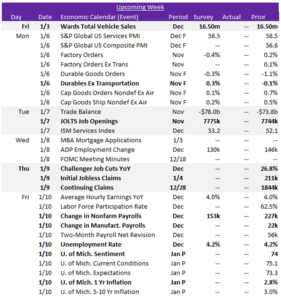

In sector specific data, December’s Wards Total Vehicle Sales are expected to hold steady at 16.50m. The final results for November’s Durable Goods Orders will be released, with Durables Ex Transportation forecasted to rise by 0.3%, which would reverse the preliminary -0.1% decline.

For the jobs report, JOLTS Job Openings are anticipated to increase slightly to 7775k in November, up from 7744k. Change in Nonfarm Payrolls for December is forecasted to decrease to 153k from 227k, while the Unemployment Rate is expected to remain unchanged at 4.2%. We will also see the results for December’s Challenger Job Cuts, alongside the weekly updates on Initial and Continuing Jobless Claims. Additionally, the preliminary results for January’s University of Michigan consumer surveys will be published.