Macro Report

Week’s Takeaway:

Data from this week continue to show that the year ended with a strong labor market and an industrial sector that was unable to find its footing.

Notes:

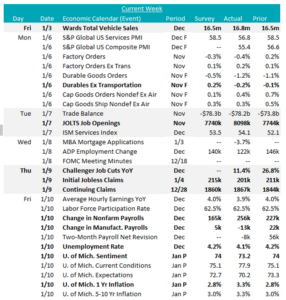

Last Friday’s Auto sector data (which is released after the market closed) helped to start this week off with some optimism. December Total Vehicle Sales blew past the estimate, signaling a seasonally adjusted & annualized rate of 16.8M units sold – an impressive figure, multiplied by the fact we have seen 4 consecutive months of increases to wrap up 2024. All that said, there are persistent concerns around the sustainability of the current momentum. Today’s University of Michigan Consumer Sentiment Survey (more below) showed that buying conditions for vehicles remain incredibly weak, while moderately improving. That, coupled with the fact that interest rates for new or used autos haven’t budged much suggests that the current flurry in activity may be marginal consumers attempting to front run any tariffs.

The final November Durable Goods report signaled weak orders from the transportation sector, with at topline MoM change to orders down -1.2%, versus an expected -0.5% print. Ex. Transportation also performed poorly, coming in at -0.2%, versus the expected 0.2% increase.

From a labor market perspective, this round of data potentially signals reacceleration from previously strong levels. November Job Openings surged to 8.1M, a 5-month high, and Initial Jobless Claims printed at 201k, their lowest level since February. All of this culminated in a robust addition in December hires, with Nonfarm Payrolls blowing past expectations of a 165k rise, up to 256k, the second consecutive month above 200k. Furthermore, the Unemployment rate dipped to 4.1%.

Following this morning’s impressive print, came a more concerning signal from the aforementioned U. of M Consumer Sentiment Survey – the topline print dipped to 73.2, below the expected print of 74, and both 1yr and long- term inflation expectations surged to 3.3% (this is the highest reading for 1yr inflation expectations since 2008).

Next Week’s Notes:

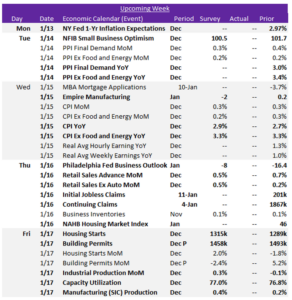

Next week, the data released will provide insights into the housing and manufacturing sectors, as well as inflation and macroeconomic trends.

The first two of five January Fed Manufacturing Surveys will be issued: the NY Empire index, expected to dip to -2 from 0.2, and the Philadelphia index, forecasted to improve to -8 from -16.4. Additionally, the December Industrial Production report will provide further context, with a consensus anticipating a 0.3% MoM increase from the prior month’s -0.1% decline, with Capacity Utilization forecasted to tick up to 77.0% from 76.8%.

Manufacturing (SIC) Production is projected to rise by 0.4%, which would further the 0.2% growth seen in November. These expected figures suggest the sector is still facing some hurdles as the path to recovery takes hold.

On the housing front, December’s Housing Starts and Building Permits are set for release, with mixed expectations. Starts are anticipated to rise to 1315k from 1289k, while Permits are forecasted to fall to 1459k from 1493k. This may be suggesting a cooling in the pace of future activity. The NAHB Housing Market Index, a gauge of homebuilder sentiment, January data will also be published.

Regarding inflation, the Producer Price Index (PPI) for December will be reported alongside the Consumer Price Index (CPI). CPI YoY is forecasted to rise to 2.9% from 2.7% in November, whereas Core (Ex Food & Energy) YoY is expected to remain unchanged at a 3.3% increase. This market expectation for Core to hold suggests that underlying inflation pressures remain contained. To offer insights into outlook, the NY Fed 1-Year Inflation Expectations in December results will be reported.

For the other macroeconomic indicators, the NFIB Small Business Optimism Index for December is projected to edge down to 100.5 from November’s 101.7, the highest since June 2021, suggesting owners may be becoming a bit more cautious about future conditions. Retail Sales December data will also be closely watched as consumer spending has been a main driver of growth. Retail Sales Advance MoM is expected to decelerate slightly to a 0.5% rise from the robust 0.7% in the prior month, while Retail Sales Ex Auto MoM are anticipated to show further gains, increasing by 0.5% from the 0.2% growth seen in November.