Macro Report

Week’s Takeaway:

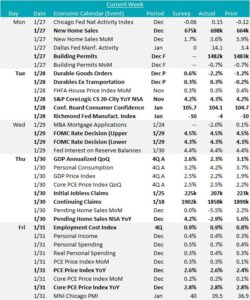

This week, the FED held rates steady, while the housing sector broadly came in better than expected. GDP for 4Q25 was also released and provides additional optimism for economic growth momentum going into 2025.

Notes:

To start the week, December new home sales beat the expected increase of 1.7% and rose 3.6% to 698k. Yearly home values measured by S&P CoreLogic came in at 4.3% for the 20 largest US cities, slightly above the expected flat print of 4.2%, further signaling that the underlying demand for housing is strong. On the other hand, pending home sales decreased -2.9% YoY, well below the expected increase of 4.2%. More than anything else, this underscore the fact that even though we are optimistic on new residential construction, the housing sector overall will be volatile.

Additionally, the preliminary Durable Goods report showed that transportation new orders significantly disappointed, down -2.2%, well below the expected 0.6% rise. Durable good ex. Transportation on the other hand came in line with the expected 0.3% rise in new orders.

On the FOMC side, there was a unanimous vote to keep Fed Funds interest rates steady at 4.25-4.5%, and a slightly more hawkish statement compared to December. In the press conference, Chair Jerome Powell highlighted the fact that the economy and labor market is in great shape, and that they believe inflation is still on a downward trajectory. On that note, Topline PCE (Personal Consumer Expenditure) rose to 2.6% YoY, in line with market expectations, while Core PCE (ex. Food & Energy) was unchanged at 2.8% YoY.

Finally, 4Q24 GDP came in at 2.3% QoQ, slightly below expectations of 2.6%, but it continues to show above potential growth. Under the hood, the consumer continues to impress, with personal consumption driving growth at the fastest pace since 1Q23. Destocking inventories was the primary drag, pushing the topline number down by 0.9%.

Next Week’s Notes:

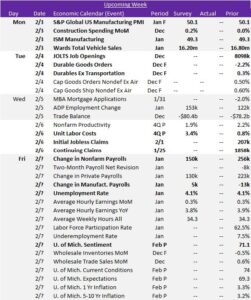

Next week, several important economic reports will be released, offering valuable insights into the manufacturing, construction, and auto sectors, along with updates on the labor market.

Key January PMI reports will be published, providing a snapshot of manufacturing sector conditions. The S&P Global US Manufacturing PMI is expected to hold steady at the preliminary estimate of 50.1. Similarly, the ISM Manufacturing PMI is forecast to remain unchanged at 49.3, continuing to indicate mild contraction. Additionally, the final report for December’s Durable Goods Orders will be released.

December’s Construction Spending report will be released, with market expectations for a modest 0.2% month-over-month increase, a recovery from the flat 0.0% change in November. Wards Total Vehicle Sales for January will also be released, with expectations for a decline to 16.20m units, down from 16.80m in December.

The January jobs report will be closely watched, with a forecasted drop in Nonfarm Payrolls to 150k from 256k in December. On the other hand, the Change in Manufacturing Payrolls is expected to rebound to 5k from December’s -13k, signaling a potential recovery in manufacturing hiring. The unemployment rate is forecast to hold steady at 4.1%, suggesting that labor market conditions remain relatively stable. Additionally, preliminary data for Unit Labor Costs in Q4 is expected to show a 3.4% increase, a sharp rise from the 0.8% increase seen in Q3, which may reflect upward wage pressures.