Macro Report

Week’s Takeaway:

This week was packed with fascinating economic releases bridging the transition between the two administrations. Industrial data broadly came in better than expectations, while a flurry of labor market data and revisions put many of the questions around whether cracks were showing to rest.

Notes:

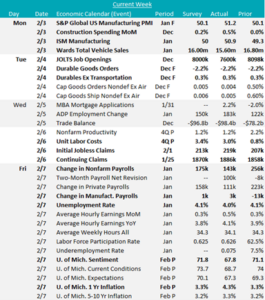

December Construction Spending figures came in strong to end the year up 0.5% MoM, above the expected increase be 0.2%. This was driven most significantly by increases in private residential spending, up 1.5%, while nonresidential spending also increased, 0.1%. YoY spending continues to expand, now for the 68th consecutive month.

In January, Wards Total Vehicle Sales dropped to 15.60m from December’s 16.80m sales, missing the expectation of a decline to 16m. This is the lowest level of sales since August. Somewhat surprisingly, auto inventories and production remain in a downtrend. We anticipate that the drawdown in inventories will lead to an uptick in steel consumption over the next couple of months but anticipate that it will be short-lived.

Manufacturing activity measured by the two prominent PMIs finally showed a breakthrough into expansion territory in January. The ISM Manufacturing PMI increased to 50.9, surpassing the market expected 49.3 and up from 49.2 in December. The S&P Global US Manufacturing PMI improved to 51.2 from the preliminary estimate of 50.1 and up from December’s 49.4.

Finally, this week provided an all you can eat buffet of labor market data. Starting with a worse than anticipated job openings figure, down to 7.6M (resulting in 1.1 openings per unemployed worker) in December. As for January nonfarm payrolls the headline figure came in at 143k, below the expected level of 175k jobs added, while the unemployment rate decreased to 4%, below the expected 4.1%. Additionally, average hourly earnings (wages) rose to 4.1% YoY, above the expected decrease to 3.8%. What was more interesting, however, was the annual benchmark revision for 2024, which signaled that many of last years perceived cracks are smaller than expected.

Next Week’s Notes:

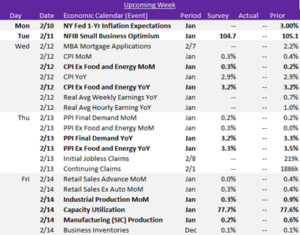

Next week, several important economic reports will be released, offering valuable insights into the manufacturing, construction, and auto sectors, along with updates on the labor market.

Key January PMI reports will be published, providing a snapshot of manufacturing sector conditions. The S&P Global US Manufacturing PMI is expected to hold steady at the preliminary estimate of 50.1. Similarly, the ISM Manufacturing PMI is forecast to remain unchanged at 49.3, continuing to indicate mild contraction. Additionally, the final report for December’s Durable Goods Orders will be released.

December’s Construction Spending report will be released, with market expectations for a modest 0.2% month-over-month increase, a recovery from the flat 0.0% change in November. Wards Total Vehicle Sales for January will also be released, with expectations for a decline to 16.20m units, down from 16.80m in December.

The January jobs report will be closely watched, with a forecasted drop in Nonfarm Payrolls to 150k from 256k in December. On the other hand, the Change in Manufacturing Payrolls is expected to rebound to 5k from December’s -13k, signaling a potential recovery in manufacturing hiring. The unemployment rate is forecast to hold steady at 4.1%, suggesting that labor market conditions remain relatively stable. Additionally, preliminary data for Unit Labor Costs in Q4 is expected to show a 3.4% increase, a sharp rise from the 0.8% increase seen in Q3, which may reflect upward wage pressures.