Macro Report

Week’s Takeaway:

Manufacturing activity has come in below expectations, but shows stead growth, while housing sales data disappointed to start the year.

Notes:

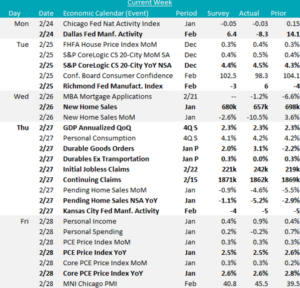

The last three of the February Fed Manufacturing Surveys were mixed. Both the Dallas and Kansas City index fell short of forecasts, -8.3 vs 6.4 and -5 vs – 4, respectively. However, the Richmond index exceeded the anticipated -3 print and increased to 6. While the manufacturing sector is improving, these results indicate it will be a bumpy path. Additionally, Durable Goods New Orders rose to 3.1%, above the expected increase by 2%. This was driven primarily by activity in the transportation sector, with the ex. Transportation portion coming in unchanged this month, below the expected slight increase of 0.3%

Housing data disappointed this week. January’s New Homes Sales missed market expectations, 657k vs 680k, and so did Pending Home Sales NSA YoY, coming in at -5.2% in January vs -1.1%. Additionally, housing prices indicated a pick-up, with S&P CoreLogic CS 20-City YoY index growing by 4.5%, surpassing the anticipated 4.4% increase and up from November’s 4.3%. The housing sector continues to be dampened by high mortgage rates and affordability issues.

The second revision of 4Q24 GDP showed no change to the topline figure at 2.3% growth QoQ, while Personal Consumption increased to 4.2% from 4.1%.

Inflation data came in line with expectations with Core PCE (ex Food & Energy) YoY declining to 2.6% and Topline PCE declining to 2.5%, also in line with expectations. FED speakers continue to express that they will be taking a cautious approach with interest rate policy in the coming months. Our view on how we expect the economy to unfold leads us to believe there will be zero interest rate cuts this year.

Next Week’s Notes:

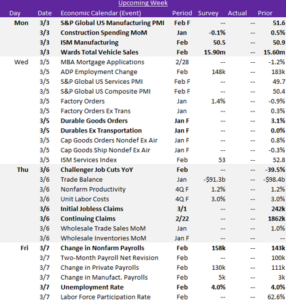

Next week will bring key data releases across the manufacturing, construction, and auto sectors, as well as a closely watched jobs report.

The final February results for the S&P Global US Manufacturing PMI will be released, which preliminary data showed an increase to 51.6 from 51.2 in January, while the ISM Manufacturing PMI is expected to edge down slightly to 50.5 in February from 50.9. Additionally, the final results for January’s Durable Goods Orders will be issued, with preliminary data indicating growth.

January’s Construction Spending is forecasted to slip by -0.1% month- over-month from the previous month’s 0.5% increase. This would end three consecutive months of expansion. Conversely, Wards Total Vehicle Sales for February are projected to jump to 15.90m from 15.60m in January, signaling expectations for a rebound in the sector.

The February jobs report will be a key focus, with Nonfarm Payrolls expected to rise by 158k, up from the 143k gain in January. The Unemployment Rate is anticipated to hold steady at 4.0%, indicating labor market conditions remain relatively stable. We will also receive data on Job Cuts, alongside the weekly updates on Initial and Continuing Jobless Claims.