Macro Report Deep Dive

Housing Market

Takeaway:

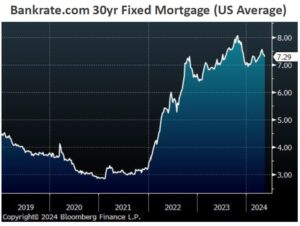

One of the major themes for 1H24 is the reset in expectations away from a swift succession in interest rate cuts and towards sustained “higher-for-longer”. Unsurprisingly, the housing market continues to be the most acutely impacted and the data has softened as mortgage rates rose since January. Taking a step back, underlying demand for housing appears stable with the starts/permits pipeline above the 2019 average, but affordability will likely remain a headwind in the 2nd half of 2024.

In April, both Housing Starts and Building Permits, underperformed against market expectations for the second consecutive month.

- Starts rose by 7%, versus a forecast increase of 8.6%. This was up from March’s downwardly revised -16.8% to an annualized rate of 1360k. Notably, starts for buildings with five or more units surged by 31.4%, while single-family units decreased by -0.4%.

- Permits declined by -3.0%, an improvement from March’s -5.0% but below the forecasted 1.6% growth. This brings the annualized rate to 1440k, down from March’s 1458k. This marks the lowest level of permits since December 2022 and is the second consecutive drop.

Notably, single-family authorization fell by -0.7% to an eight-month low of 9770k, while buildings with five or more units slumped by -7.6%.

For May, the NAHB Housing Market Index fell to 45, the lowest in four months, down from 51 in April and below market expectations of 51. This marks the first decline in builder sentiment since November 2023, attributed to mortgage rates consistently above 7% for the past month. The index for current sales conditions fell six points to 51, the sales expectations component for the next six months dropped nine points to 51, and the measure of prospective buyer traffic decreased by four points to 30.

For April, Existing Home Sales fell by -1.9% to an annual rate of 4.14m units, the lowest in three months. This compares to an upwardly revised 4.22 million units in March and forecasts of 4.21 million.

Similarly, New Home Sales declined by -4.7% to an annualized 634k, coming in well below projections of 680k. March was also revised down to 665k.

The drag in housing is likely the result of a steady increase in mortgage rates from early-March, through the end of April coupled with limited supply. However, as of the week ending May 17th, MBA Mortgage Applications rose by 1.9%, following a 0.5% increase the previous week, marking the third consecutive week of growth. This increase aligns with the decline in the MBA 30-Year Mortgage Rate, which fell to 7.01% in the same week, reaching a five-week low, as hopes for lower inflation reduced long-term Treasury yields.