Fundamental Report

Supply-Side Takeaway:

Domestic supply remains surprisingly restrained, while expectations of decreasing US prices are dimming the appeal of Q2 imports.

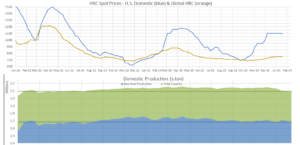

The spread between Domestic – Global spot prices contracted further due to a decrease in the domestic price rather than an increase in the global price, which remained stable. Meanwhile, US domestic production showed little change.

Notes:

- The global HRC spot price edged a bit higher but stayed at $747, with $9 increase in Europe being slightly offset by a $6 decrease from Turkey, and -$1 from both China and Korea.

- The Domestic – Global HRC spread fell to $342 and is currently in a 6-week decline.

- For the week ending on January 20th, capacity utilization ticked down by 8% to 75.7%, and domestic raw steel production fell to 1.682m net tons – the lower end of the October-Current range.

Demand-Side Takeaway:

The S&P Global US Manufacturing PMI showed a signal of support, increasing to 50.3, the highest level since October 2022. Despite this, manufacturing activity appears muted as evident by the more reliable FED surveys, and the most recent ISM Manufacturing PMI.

- January preliminary data for the S&P Global Manufacturing PMI unexpectedly rose to 3 from December’s 47.9, beating market expectations of a further decline to 47.7.

- Fed Manufacturing Surveys headline average for December was -7.12, with January survey data so far being NY Empire plunging to -43.7, Richmond falling to -15 from -11, and Philadelphia rising by 2.2 to -10.6.

- ISM Manufacturing PMI slightly improved in December, rising to 4 from November’s 46.7, and beat market expectations of an increase to 47.1.