Fundamental Report

Supply-Side Takeaway:

Domestic production continues to climb, while US prices lose upward momentum, and our adjusted global spot price broke below $700 for the first time in nearly 6-months.

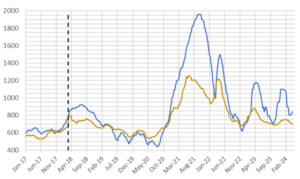

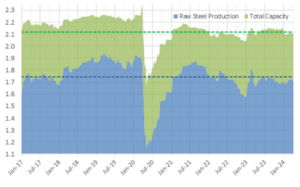

The Domestic – Global HRC price differential expanded further, mainly due to the domestic spot price increasing, while the global average continued to steadily decline. For imports, March’s arrivals were revised a bit lower, but continue to point to a level not seen since August 2022. Meanwhile, the domestic production jumped up, rising to the historical average level for the first time since August 2023.

HRC Spot Prices – US Domestic & Global

- The global HRC spot price fell to $694 from $703, marking the tenth-consecutive week of declines. This week the decrease was primarily due to Europe and Turkey both dropping by $22.

- The Domestic – Global HRC spread widened further, expanding by $24 to $141, climbing back to levels last seen in February.

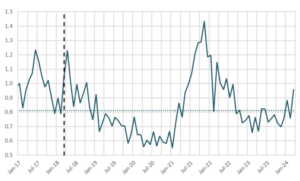

Total Sheet Imports (s.ton)

- Imports estimated sheet arrivals for March point to a level of 960k, a jump up from February’s notable slump in arrivals, dropping down to 758k.

- Supply chain issues and shipping delays could be the reason for the February dip, but preliminary data is still showing an overall trend higher in imports.

Domestic Production (s.ton)

- For the week ending on April 6th, capacity utilization ticked up by 1.1% to 78.6% and domestic raw steel production rose to 745m from 1.722m/tpw, reaching the highest level since August 2023.

- This brings the year-to-date production to 23.497m, operating at a rate of 4%, -2.4% below this point last year.