Fundamental Report

Supply-Side Takeaway:

Domestic production cuts are being offset by continued elevated import arrivals. Global prices continue to deteriorate, while recent price announcements have frozen domestic prices in place over the last 3 weeks.

This week, the U.S. Domestic – Global price differential widened further, driven by an increasing US domestic price, and continued declines in the global average price. For imports, preliminary data for February arrivals continues to suggest a slight reduction in imports, followed by a notable increase to March’s arrivals. Meanwhile, US domestic production pulled back further, reaching its lowest level in 2 months.

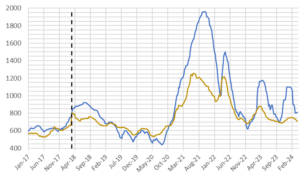

HRC Spot Prices – US Domestic & Global

- The global HRC spot price fell to $708 from $713, primarily due to a $18 decrease from Turkey and a $15 decline from Europe, while China experienced a nearly $7 increase.

- The Domestic – Global HRC spread widened, expanding by $15 to $102, breaking back through to the $100 level and marking the third consecutive week of expansion.

Total Sheet Imports (s.ton)

- Imports estimated sheet arrivals for March point to a continued trend higher, rising to 1,069k from February’s estimated slight slump in arrivals of 840k. This week’s preliminary data for March, if realized, would reach the highest level of import arrivals since March 2022.

- Supply chain issues and shipping delays could be the reason for the February dip, but preliminary data is still showing an overall trend higher in imports.

Domestic Production (s.ton)

- For the week ending on March 23rd, capacity utilization ticked down by 0.5% to 76.7% and domestic raw steel production fell to 703m from 1.714m/tpw, continuing to scale back.

- This brings the year-to-date production to 20.010m, operating at a rate of 0%. This marks a -2.9% decrease from the same timeframe in the previous year, when production was at 20.605m with a capacity utilization rate of 77.7%.