Macro Flash Report

FOMC RATE DECISION

Takeaway:

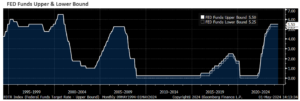

While the FOMC is leaving rates unchanged at 5.25-5.5%, today’s statement is signals that the FED is taking a longer view on inflation trends while acknowledging that the recent data is coming in hotter than they initial anticipated. Leading up to the statement and press conference, the market was anticipating a hawkish turn (i.e., less rate cuts, also starting later) and that is exactly what was delivered. We still maintain the belief that July will be the first cut, but also believe that will be the only cut in 2024.

The FOMC Rate Decision today to hold interest rates comes amidst a backdrop of resurgent inflation and a labor market that remains stable, which has impacted the market expectations for cuts. The market now only sees two rate cuts over the next year, translating to a total of 50 basis points of rate cuts through till April 2025, with the expectation that the first cut will occur at the November meeting.

Inflation & the Labor Market

Recent inflation indicators have underscored a notable resurgence in inflation, with prices heating up more than the market had already anticipated. The CPI YoY escalated to 3.5%, higher than the anticipated 3.4%, while the Core CPI (Ex Food & Energy) remained at 3.8% versus expectations of a slight decrease to 3.7%. The PPI (Ex Food & Energy) YoY also reflected higher-than-expected inflation, recording a 2.4% increase against a forecast of 2.3%. This pattern of persistent price increases was also confirmed in the Core PCE YoY Deflator – the most closely watched gauge of inflation for the FED – when prices rose 2.7% versus the market estimated 2.6%. Further compounding inflation concerns, the April final reading of the University of Michigan consumer sentiment survey revealed a rise in 1- yr inflation expectations to 3.2% from the preliminary reading of 3.1%, marking the highest level since November. Due to these developments and the fact that the disinflationary base effect from Fall/Winter 2023 is going to roll off, attention is increasingly turning to the labor market as a critical indicator for the timing of interest rate cuts. As it stands, the labor market remains stable, although some signs of cooling will be closely watched in the data set to be released this Friday.

Market Expectations (immediately following the decision)

Due to the resurgence in inflation and a still stable labor market, market expectations for interest rate cuts have notably changed. The tables below highlight those notable swings for two of the more discussed months, July and September. Another interesting development for these market expectations is that as of today they started including probabilities for hikes.