Macro Flash Report

May’s Fed Manufacturing Surveys

Takeaway:

May’s Fed Manufacturing surveys improved slightly but remain in an overall contractionary position. Forward looking expectations largely remain optimistic, however, slightly less than in April. The ongoing recovery in the manufacturing sector continues to be sluggish as industrial sectors of the U.S. economy continue adjusting to a higher for longer interest rate environment.

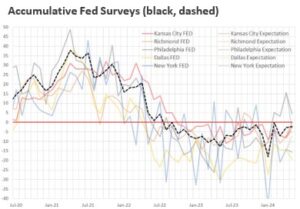

NY Empire dropped to -15.6 from -14.3, underperforming against market expectations of -10.3, marking the sixth consecutive month of contraction.

- New orders fell (-16.2 to -16.5), backlogs shrank (-10.1 to -1), while shipments stabilized (-14.4 to -1.2).

- Labor market conditions continued to be weakened, while the rate of increase in input and selling prices showed slight

- Despite ongoing challenges, firms’ six-month expectations dipped but remained hopeful (16.7 to 14.5).

Philadelphia remained in expansion but declined to 4.5, down from a two-year high of 15.5 in April and short of the anticipated 7.8.

- New orders (12.2 to -7.9) and backlogs (0.8 to -11.5) turned negative for the first time since February, and shipments went negative (19.1 to -1.2) for the first time since January.

- Employment and hours improved but stayed in contraction, while the price indexes overall increased but were below long- term averages.

- Firms maintained a positive outlook for growth over the next six months (34.3 to 32.4), though slightly less optimistic.

Dallas fell to -19.4 from -14.5, a four-month low and below the forecasted -15.

- Production (4.8 to -2.8) and shipments (5 to -3) reduced, whereas new orders (-5.3 to -2.2) and backlogs (-5.9 to -3.1) showed minor improvements.

- Employment declines and shorter workweeks were Prices decreased while costs rose.

- Six-month expectations (7.9 to -3.3) notably

Kansas City improved to -2 from -8, beating the expected -7, showing the mildest contraction since December 2023 in its ninth consecutive negative month.

- New orders dropped (-6 to -13), but reductions in backlogs (-18 to -19) supported a rise in shipments (-11 to 8).

- Employment grew despite a decline in the average Price pressures persisted.

- Firms’ growth expectation in the next six months improved (2 to 6).

Richmond rose to 0, improving from -7 and surpassing the anticipated -2, marking the highest reading in seven months.

- Shipments notably rebounded (-10 to 13) and new orders slightly improved (-9 to -6), while backlogs worsened (-17 to – 19).

- Employment experienced a sharper decline, while price dynamics shifted.

- Firms’ optimism remained relatively stable (6 to 3).