Macro Report

Week’s Takeaway:

While manufacturing continues to show an uneven recovery and the labor market continues to cool, robust housing market growth and a strong consumer provide an optimistic outlook for the economy’s overall trajectory.

Notes:

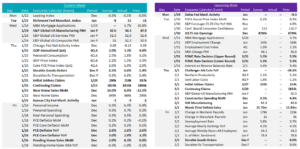

Manufacturing data continues to provided a mixed view on the potential for a near-term industrial recovery. The January readings for Richmond & Kansas City FED Manufacturing Surveys both came in below expectations, – 15 vs -8, and -9 vs -3, respectively. The Richmond print was concerning, with expectations of an improvement versus an actual print at its lowest level since February 2023, while KC, which had been showing signs of recovery,

fell much further than anticipated. On the other hand, January’s preliminary S&P Global US Manufacturing PMI index printed significantly above market expectations and improved from the prior month, 50.3 vs 47.6, and 50.3 vs 47.9.

The housing market was further buoyed by December’s New Home Sales and Pending Home Sales, which both showed increased growth, 8.0% vs – 12.2%, and 8.3% vs 0.0%. This was a strong signal for future activity, with pent-up demand clearly coming to the market as the 30-year rate continues to ease.

Another blockbuster datapoint was the preliminary data for 4th Quarter GDP Annualized QoQ, which showed an expansion of 3.3%, far surpassing the anticipated 2.0% growth. While this represents a decrease from the previous 4.9%, it still indicates significant economic growth. Furthermore, the PCE Core Deflator, a key inflation indicator, rose by just 2.9%, below the forecasted 3.0% and reaching its lowest rate since March 2021.

In contrast, the preliminary December Durable Goods Orders was less encouraging, showing no growth at 0.0%. This was a stark change from the 5.4% increase seen in November and fell short of the expected 1.5%.

Initial and continuing claims both came in above expectations, 214k vs 200k, and 1,833k vs 1,823k, respectively. This is a clear signal that the labor market is cooling, with initial claims rebounding significantly from the 16-month low touched the prior week.

Next Week’s Notes:

Next week, we are set to receive a comprehensive set of early-month data, which will shed light on various economic sectors. Our key focus areas include manufacturing, construction, automotive, and the labor market.

January’s ISM Manufacturing PMI is highly anticipated as the manufacturing sector has been displaying mixed signals in its recovery. Current market expectations are for a slight easing to 47.3, just under the previous month’s upside surprise to 47.4. In construction, December’s Spending is forecasted to show a modest increase, moving up to 0.5% MoM from 0.4%, where the main driver of growth was from the private spending residential segment.

For the auto sector, January’s Wards Total Vehicle Sales have a 15.70m projection, a decline from December’s 15.83m, which was the highest sales amount since July 2023. Additionally, although sales have not fully recovered to the levels seen before the pandemic, there has been a clear upward trend forming since 2022.

Finally, a slew of labor market data is due, including JOLTS Job Openings, Challenger Job Cuts, and Change in Nonfarm Payrolls. These will be the most anticipated for insights on worker demand, which have been showing signs of easing. Job Openings is expected to decline further, falling to 8700k from 8790k, which marked the lowest level since March 2021. Change in Nonfarm Payrolls is also forecasted to see a decline, dropping to 178k from 216k.