Macro Report

Week’s Takeaway:

This week’s industrial data highlighted the uneven recovery as these sectors face strong headwinds. In contrast, the strength in recent labor market data (albeit potentially overstated) suggest that the window has likely closed for pre-election rate cuts.

Notes:

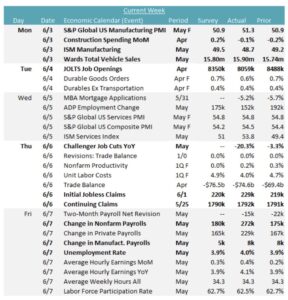

In the recent manufacturing data, the S&P Global US Manufacturing PMI exceeded expectations, rising to 51.3 versus the expected 50.9. Conversely, the ISM Manufacturing PMI dropped to 48.7, surprising to the downside as was anticipated for a slight increase to 49.5.

Construction Spending MoM disappointed for the fourth consecutive month, slipping by -0.1% instead of the forecasted 0.2% increase. This decline was mainly due to a -0.2% decrease in public spending and a -0.1% fall in private spending. However, residential spending edged up by 0.1%.

Wards Total Vehicle Sales surpassed expectations of 15.80m and jumped to 15.90m from April’s 15.74m. This marks the third straight month of sales growth. However, sales have still yet to consistently reach the pre- pandemic levels of 16-17m.

The latest labor market data presents a complex picture. Nonfarm Payrolls surged by 272k in May, the highest in five months and well above the forecasted 185k, reflecting robust hiring. Manufacturing Payrolls also beat expectations, holding steady at 8k instead of the predicted decline to 5k. Meanwhile, Challenger Job Cuts for May decreased significantly by -20.3% year-over-year, the lowest since February 2021.

Despite these positive indicators, the Unemployment Rate rose to 4.0%, up from the forecast to stay at 3.9% and reaching the highest level since January 2022. This increase, alongside the sharp drop in JOLTS Job Openings to 8059k, well below the anticipated 8350k, signals potential challenges in labor demand.

The divergence between rising payrolls and unemployment suggest that the true state of the labor market likely lies between these mixed readings, indicating a resilience but also cooling underlying structural changes.

Next Week’s Notes:

Next week, key inflation data will be released, including May’s CPI YoY and CPI (Ex Food & Energy) YoY. CPI is expected to remain steady at 3.4% year- over-year, while the CPI (Ex Food & Energy) is forecasted to decline slightly to 3.5% from 3.6%. Additionally, May’s PPI (Ex Food & Energy) is projected to drop to 0.3% month-over-month, down from 0.5%. Consumer expectations for inflation will also be evaluated through May’s NY Fed 1-Yr Inflation Expectations and preliminary June data from the University of Michigan consumer surveys.

Also of note, the FOMC will meet and decide on interest rates. While the FED Funds Upper & Lower Bound will likely be unchanged at 5.5-5.25%, the SEP (Summary of Economic Projections) will also be released. Here, we will get an update to the dot plot which was still showing 3 cuts for 2024 as recently as March.